DC Professionals: Income in

Workplace Retirement Plans

DC Professionals: Income in

Workplace Retirement Plans

Deb Dupont

Assistant Vice President, Workplace Retirement Research

LIMRA and LOMA

April 2024

Retirement income, and how to use defined contribution (DC) plans to help individuals generate it, is a critical topic in the retirement industry and to the individuals DC plans serve.

Many voices and opinions are part of this discussion, from providers to advisors to plan sponsors to industry thought leaders and more. In the fall of 2023, LIMRA undertook a brief scan of the professionals engaged in the development, sales and study of these products. We asked them to share their philosophies about retirement income in general, guaranteed retirement income in particular, and the role of various entities and solutions in helping address the income issue.

We distributed an electronic survey via targeted email and LinkedIn post to industry thought leaders and LIMRA members who work for record keepers, distributors, asset managers, law offices and even fellow researchers with whom they work. Participants were invited to share the survey with colleagues who are engaged in the DC industry. Forty-five DC industry professionals from 24 organizations responded. Unlike most of our more formal research efforts, this was not a random sample, and it was not representative of any specific subset of the profession. What this exercise does do, however, is offer up a qualitative diversity of insights and opinions about the income space and solutions from people who are deeply engaged in product development and/or distribution of DC plans and services.

There is widespread agreement among the respondents that making sure participants have adequate retirement income is an industrywide problem (just two respondents disagreed to any extent, while another two were neutral). The majority of respondents — 92 percent — were pretty evenly split between those who agreed strongly and those who simply agreed.

There’s less agreement about how to tackle the issue. About half of the respondents agree that a “guarantee” must be part of the solution, but only about a quarter feel strongly about that matter. On the other hand, slightly less than 1 in 10 actively disagree about the necessity of a guarantee. The rest (about a third) are neutral, which means that the glass is half full for champions of guaranteed income solutions.

Conversely, we did find greater consensus, about 90 percent agreement, that there’s room for both guaranteed and nonguaranteed solutions in DC plans.

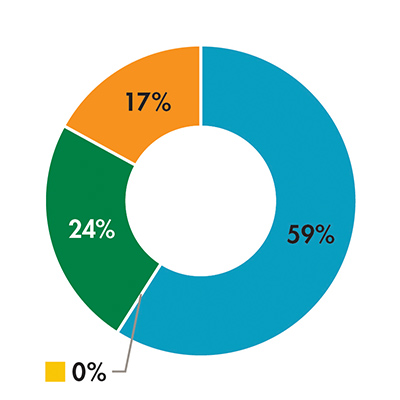

Whether income solutions belong in DC plans is not a universal assumption. The role of a DC plan is to help participants amass a pool of wealth from which to generate retirement income; the role of a DC plan in helping participants create an income stream is less clear. Twenty-four of the 41 respondents who answered the question agreed that in-plan is “the best location for an income solution for the average middle-income worker:” Ten responded that the best place is a rollover individual retirement account (IRA); none selected retail brokerage, while “other” was chosen by seven respondents.

There’s a strong but not surprising disconnect between the thoughts of the survey respondents who represent a cross section of services within the industry, and those of DC advisors themselves (Figure 1). Advisors are much more likely to consider IRA rollover and brokerage account solutions — which they presumably have a role in selling — to be appropriate for average income investors.

■ Retirement Plan ■ Retail Brokerage Account ■ Rollover IRA ■ Other

|

|

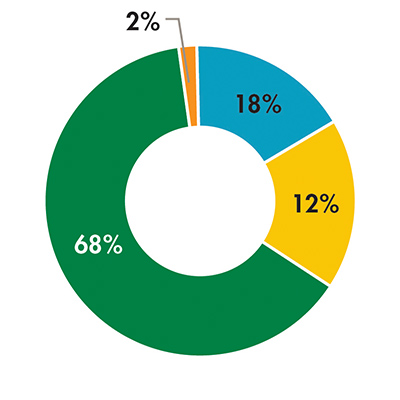

We also asked survey respondents which industry player or entity is most responsible for helping individual participants make the transition from investment to income. By a wide margin, most assign the highest responsibility to personal financial advisors — 36 to 41, while the remaining five assign medium responsibility to personal advisors (Figure 2).

The assumption that financial advisors should be on the hook to help individuals create income streams creates both a challenge and opportunity for DC stakeholders. Research consistently shows that personal financial advisors are utilized by only about a third of individuals, and usually by those who are older and/or have greater income and net worth. The need to use a DC investment to create retirement income, however, is a more universal challenge and likely more pressing for middle-income (i.e., not high net worth) individuals, pointing to a need for more scalable, perhaps technology- and/or artificial intelligence (AI)-driven, solutions.

Filter the data in this chart by clicking on a color bar in the chart legend.

This space is ready for innovation, both guaranteed and nonguaranteed. In the wake of SECURE 1.0 and 2.0, we are seeing new constructs and partnerships for in-plan and out-of-plan solutions. What most participating respondents agree on is that we will see more moderate than dramatic growth in adoption of both guaranteed- and nonguaranteed income solutions within DC plans over the next three to five years.

Few felt that more regulation or legislation will help expand this market; several cited the need for income solutions to be attached to qualified default investment alternative options (QDIAs).

One commented, “We need to create alignment between record keepers and advisors/consultants that helping the participant solve their income needs will lead to growth for all industry participants. It doesn't need to limit the rollover opportunity that advisors are targeting.”

Comments were wide ranging and are well worth taking a look at in the summary report.

LIMRA research will continue to explore how the DC industry — and DC plans themselves — support the growing need for retirement income for the increasing number of Baby Boomer and Gen X (and beyond) retirees. Product developments and designs, investments and new technologies will undoubtedly become part of the conversation about how retirement income — guaranteed or otherwise, in-plan or otherwise — will help future retirees use their DC experiences to create their own retirements.

Out of plan: 41%

Out of plan: 41% Out of plan: 82%

Out of plan: 82%