A recent LIMRA report sheds light on how multiple-line agents—who are affiliated with one company and primarily sell auto, home or other property and casualty insurance—feel about selling life insurance products, lead generation, and opportunities for future growth.

Multi-line agents derive most of their business from selling property and casualty products. Some agents, however, have incorporated life insurance products, and to a lesser extent annuities and investment products, into their practices. Yet, on average just 14% of a multi-line agent’s income is from life insurance.

Multi-line agents are unique in the financial services industry because they:

- Primarily serve the middle market—three-quarters of their clients have household incomes below $125,000

- Have lots of clients—on average, multi-line agents’ client base is at least double that of all other types of financial professionals

- Serve/have relationships with all generations

- Have clients seeking them out for property and casualty products

According to the 2019 Insurance Barometer Study, 41% of middle market Americans are uninsured. Multi-line agents have the opportunity to help their middle-market clients address their life insurance and retirement planning needs, including products that provide guaranteed lifetime income like annuities. Their existing relationship puts them in an ideal position to help by offering these services because they have already established a trusted relationship with these clients. Prior LIMRA research has shown that the top factor influencing consumers to purchase life insurance is trust in their advisor.

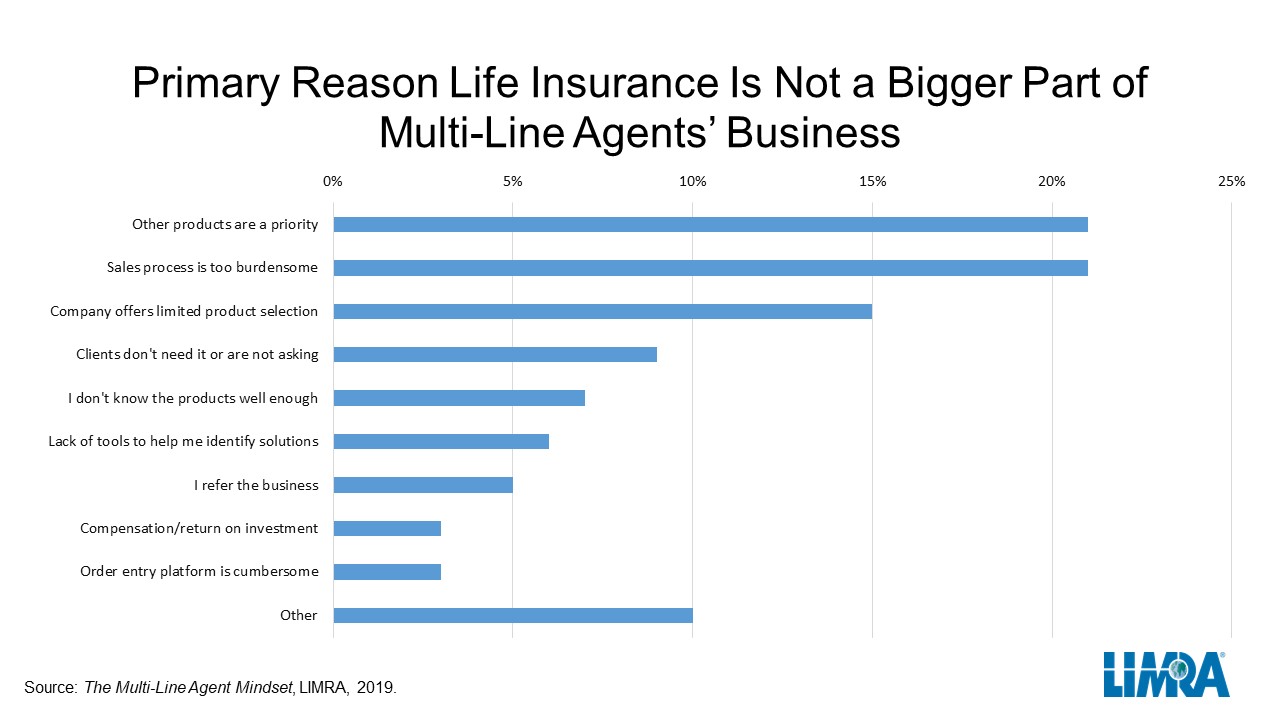

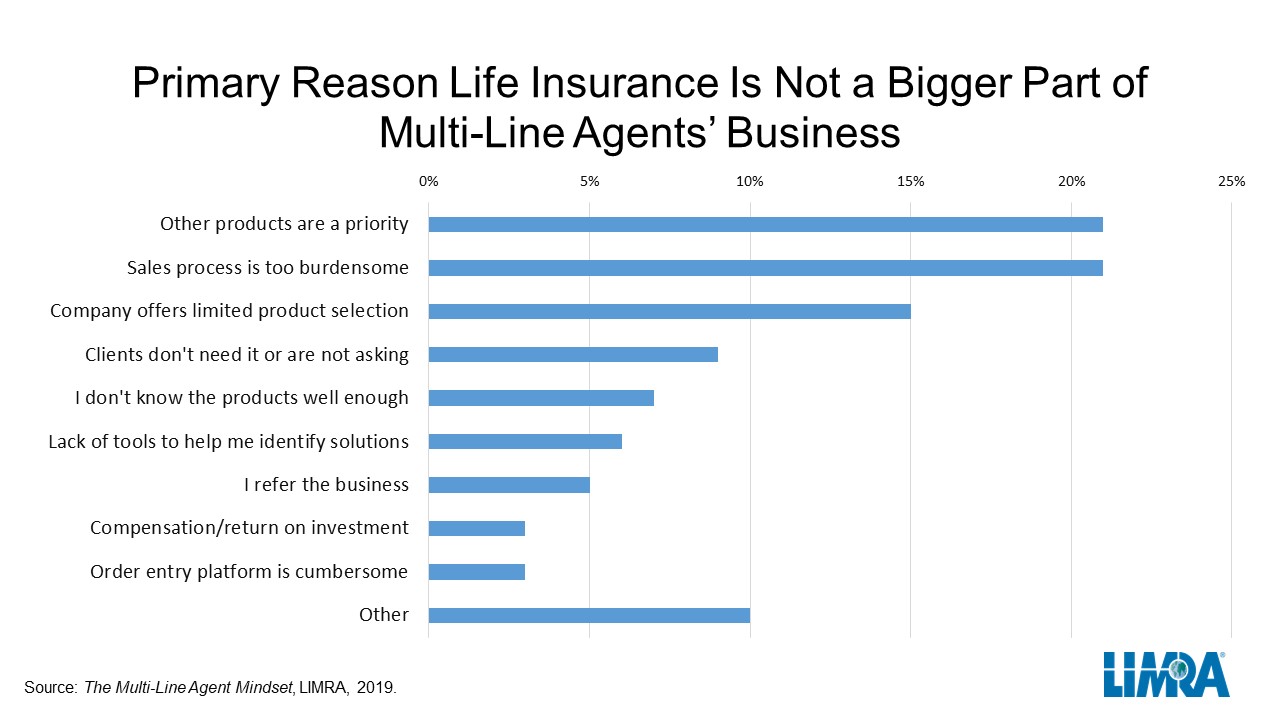

Agents say that the primary reason life insurance isn’t a bigger part of their practice is that other products are a priority and the sales process is burdensome. The selection of product offerings also plays a role (see chart below).

Many companies offer services and support in an effort to help their agents sell life insurance. The support tools multi-line agents in the study identified as being most important were analytical tools to help prioritize opportunities/leads; digital tools to identify client solutions; and modeling tools on life insurance strategies.

Looking toward the future, multi-line agents see technology as both a challenge and an opportunity. Those reluctant to sell life insurance are twice as likely to view competition from online purchasing platforms as an issue than those more inclined to sell life insurance. LIMRA research suggests multi-line companies could alleviate these concerns by leveraging technology to help their middle-market clients with their financial and retirement planning needs (either through their agencies or from the home office), providing a unique value proposition, and at the same time, strengthening the company-agent and company-client relationship.