According to the new Secure Retirement Institute® (SRITM) study, more than half (56%) of U.S. workers are interested in investing in a guaranteed lifetime income option within their employer’s retirement savings plan if it was available to them. Of those who are currently saving in their employer’s defined contribution (DC) plan, 61% say they would be somewhat or very likely to contribute to a guaranteed lifetime income investment option.

Prior to the SECURE Act of 2019 being passed, there were significant factors hampering in-plan guarantee adoption. From the plan sponsor’s perspective, there were fiduciary concerns about choosing an annuity provider and the long-term liability of that choice. From an employee’s perspective, in addition to the lack of access to this option, the inability to move the annuity to a new plan if the employee switched jobs deterred employees from choosing this option.

The recently passed SECURE Act of 2019 makes it easier for DC plan sponsors to offer lifetime income options to their participants. The new law creates a safe harbor for employers that add an in-plan annuity to include as an investment within a DC plan, with new provider-selection rules.

The SECURE Act also increases the portability of an in-plan annuity by:

- Allowing employees who take another job or retire move their annuity to another 401(k) plan or to an IRA without surrender charges and fees; or

- Move their annuity investment to an IRA if their company no longer offers that option in their plan.

Younger Workers Have Greater Interest for Guaranteed Lifetime Income

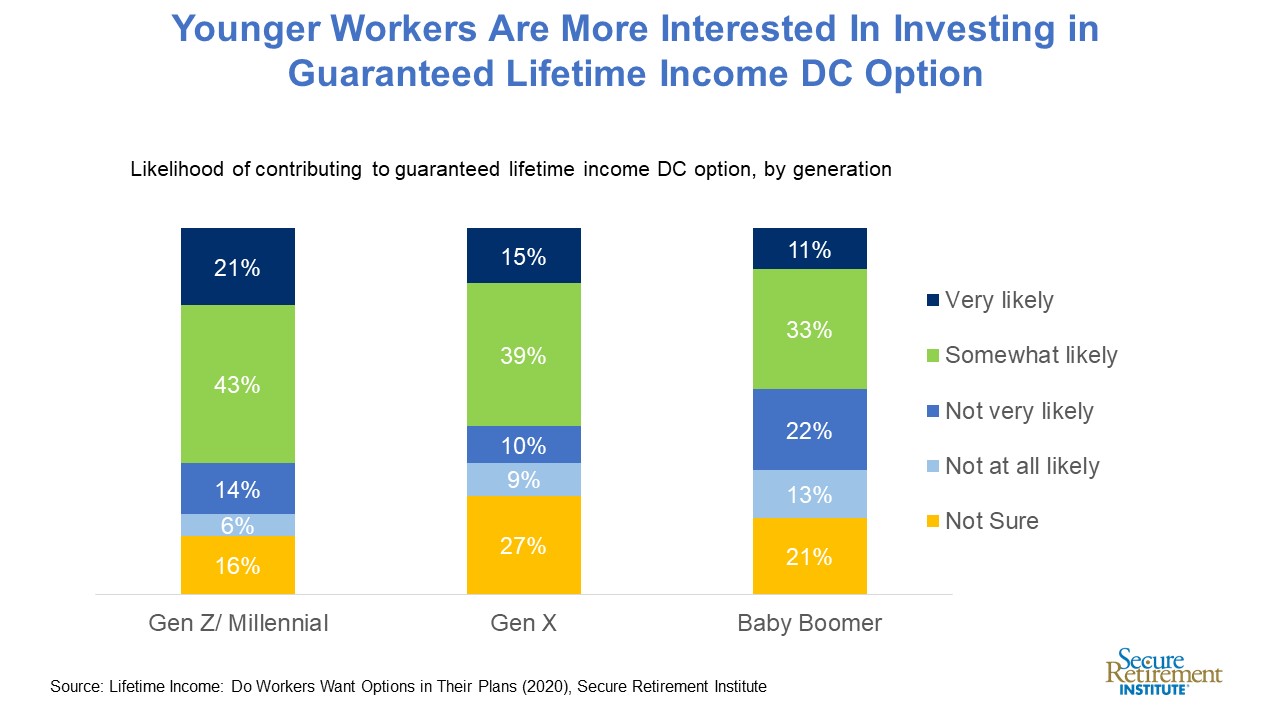

The SRI study finds younger workers are more open to guaranteed lifetime income investments, like an annuity. Nearly two-thirds (64%) of adult Gen Z/Millennial workers say they are somewhat or very likely to contribute to this option, compared with 52% of Gen X and 42% of Baby Boomer workers (chart).

Younger workers are the least likely to have pensions, and thus would benefit more from lifetime income. In fact, nearly half (47%) of Millennial workers expect their employer retirement plan savings to be their primary source of income when they retire.

Knowledge about annuities also plays a role. Forty-six percent of workers with poor annuity knowledge (as measured by 10 annuity knowledge questions provided in this study) are somewhat or very likely to invest in an in-plan annuity, compared with 64% of those in the high knowledge category. Like many optional features in DC plans, participant inertia is hard to overcome. Unless the income solution is made the default investment, educating workers will be critical to greater adoption.

Workers Value the Security Guaranteed In-plan Annuities Offer

Almost 4 in 10 workers consider the financial security of lifetime guaranteed income and knowing how much income they’ll receive in retirement as the top advantages of a guaranteed lifetime income option in their employers’ retirement savings plans. SRI finds younger workers are attracted to the idea of being able to start planning for income before retirement. Thirty-six percent of Gen Z/Millennial workers say it’s an advantage versus 31% of Gen X workers and 27% of Baby Boomers.

Today less 1 in 5 workers under age 50 have access to a pension, which can provide guaranteed lifetime income in retirement. In-plan annuities offer that lifetime protection many workers want. SRI expects the SECURE Act will make it easier for workers to access that through their workplace retirement savings plan.