In March 2020, Congress passed the Coronavirus Aid, Relief and Economic Security (CARES) Act to help Americans manage the sudden economic fallout of the coronavirus outbreak and ensuing widespread unemployment.

Some of the Act’s provisions have the potential to deeply impact defined contribution (DC) retirement programs by expanding how workers can tap in to their retirement savings when affected by the virus and/or crisis. For eligible workers, CARES doubles the amount that can be taken as a loan, from $50,000 to $100,000. It also creates a new category of plan withdrawal, without the 10% penalty associated with traditional hardship withdrawals. A CARES withdrawal also allows the individual to pay taxes over a three-year period rather than in a single tax year.

The availability of the options is contingent upon whether the plan itself allows loans and/or hardships, and plans must be amended by plan sponsors to enable the new withdrawal options and limits. The Secure Retirement Institute® (SRI®) recently surveyed plan sponsors about their familiarity with these CARES provisions and their needs and expectations of their plans’ providers relative to understanding how the Act affects their own plans.

The study found 8 in 10 DC plan sponsors are familiar with the CARES Act and its retirement provisions. Private sector businesses are more likely than not-for-profit organizations to be familiar with the CARES Act (81% versus 61%).

While they may be familiar with the Act, sponsors may be less versed in the potential impacts for their plans and on participants’ longer-term savings. A little more than half of plan sponsors (51%) feel, at least to some extent, that they would benefit from guidance from their DC plan’s recordkeeper in understanding how CARES may affect their plan.

“Sponsors in the smallest and largest plans are less likely to look to recordkeepers for this help, although possibly for quite different reasons,” said Deb Dupont, associate managing director, SRI Institutional Retirement Research. She notes that mega plan sponsors likely have robust on-staff plan and legal resources of their own. Sponsors of the smallest plans may simply not appreciate the potential implications for their retirement plans and employees.

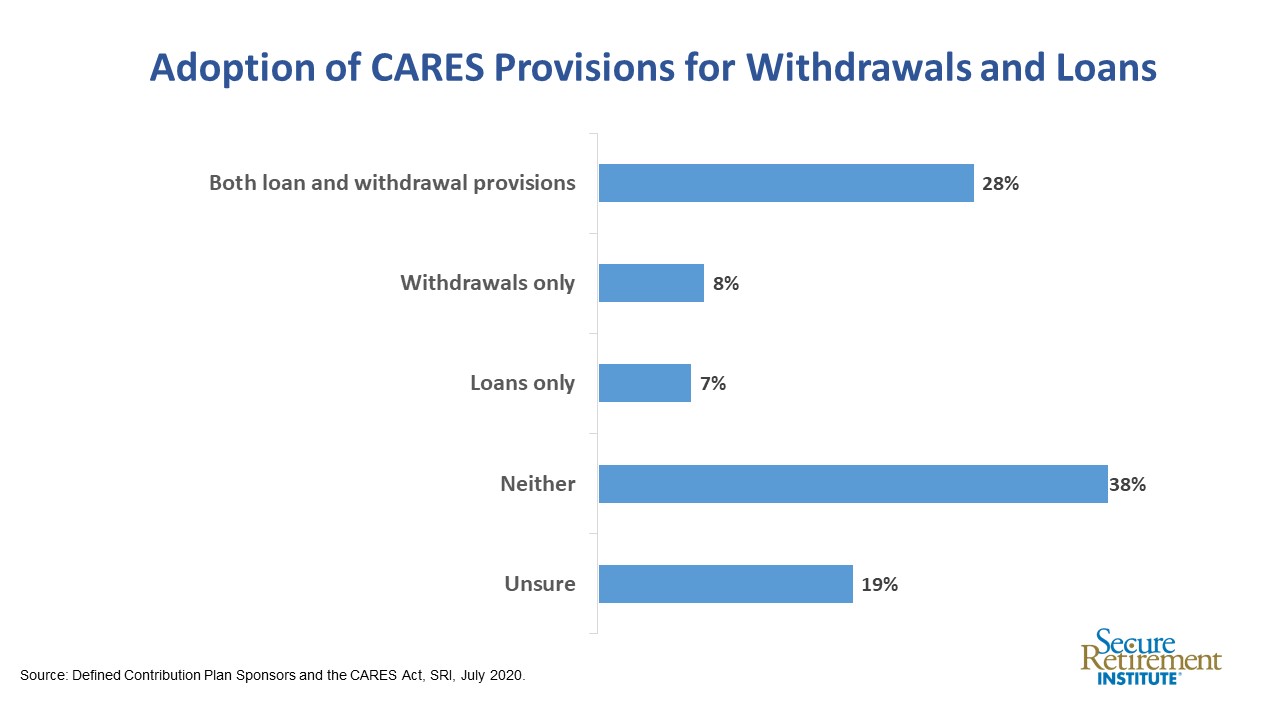

Whether or not to adopt the withdrawal and/or loan provisions of the CARES Act is at the discretion of each plan sponsor. Nearly 4 in 10 (38%) do not plan to implement the expanded withdrawal capability or the increased loan capability.

Another one fifth (19%) are unsure at this point, leaving 43% who do plan to amend their plans to offer at least one withdrawal update enabled by CARES.

The likelihood of accommodating CARES-enabled distributions increases with plan size; the largest plans are significantly more likely to have acted or plan to act to increase withdrawal options for their participants. Plan recordkeepers may be able to leverage experiences and “lessons learned” from larger plan rollouts when guiding smaller plan sponsors in reacting to CARES provisions and in determining whether they are right for specific plans and plan sponsors.