The COVID-19 pandemic resulted in rapid and unprecedented changes in the annuity industry. Business practices quickly changed as the industry went remote, and it is likely the changes adopted in 2020 will continue as the new normal for the industry.

New research from the Secure Retirement Institute® (SRI®) asked advisors about their perspective on the annuity sales process and how it could be improved.

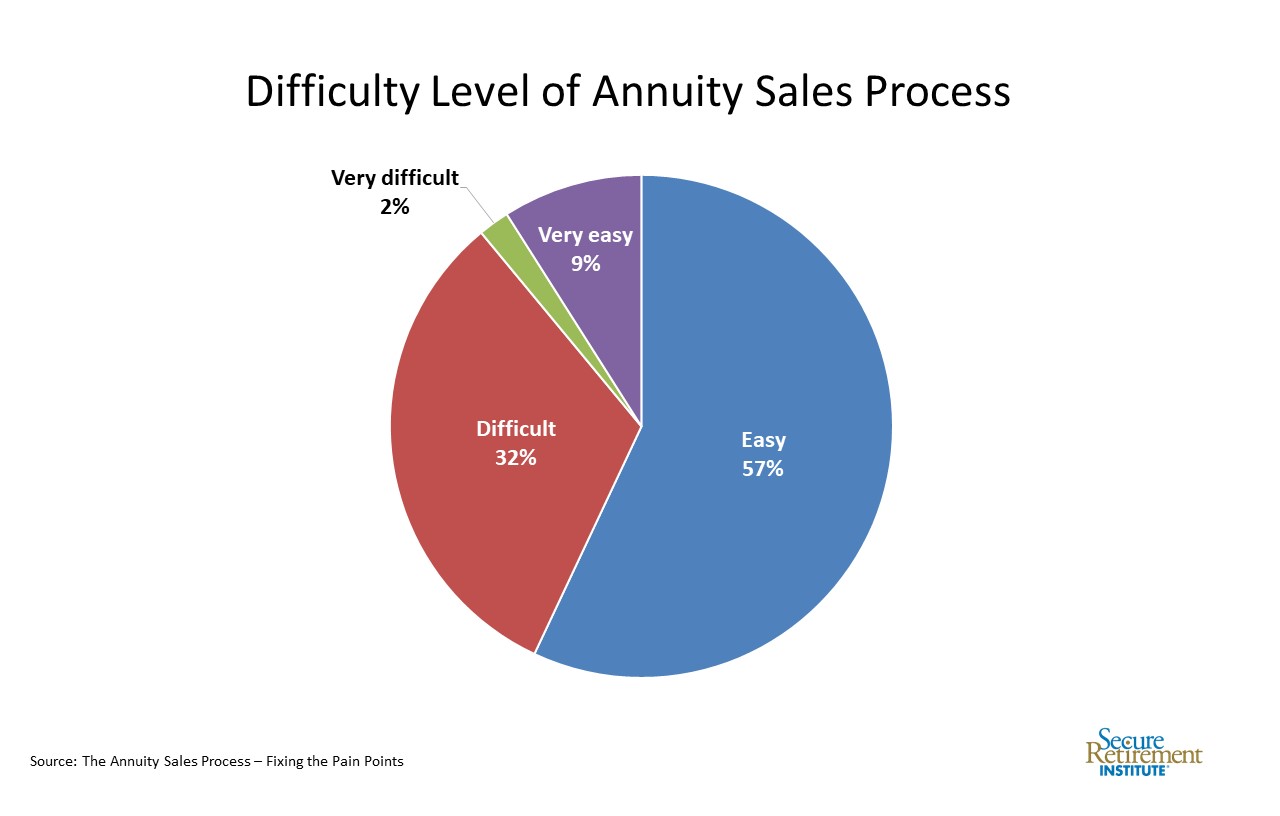

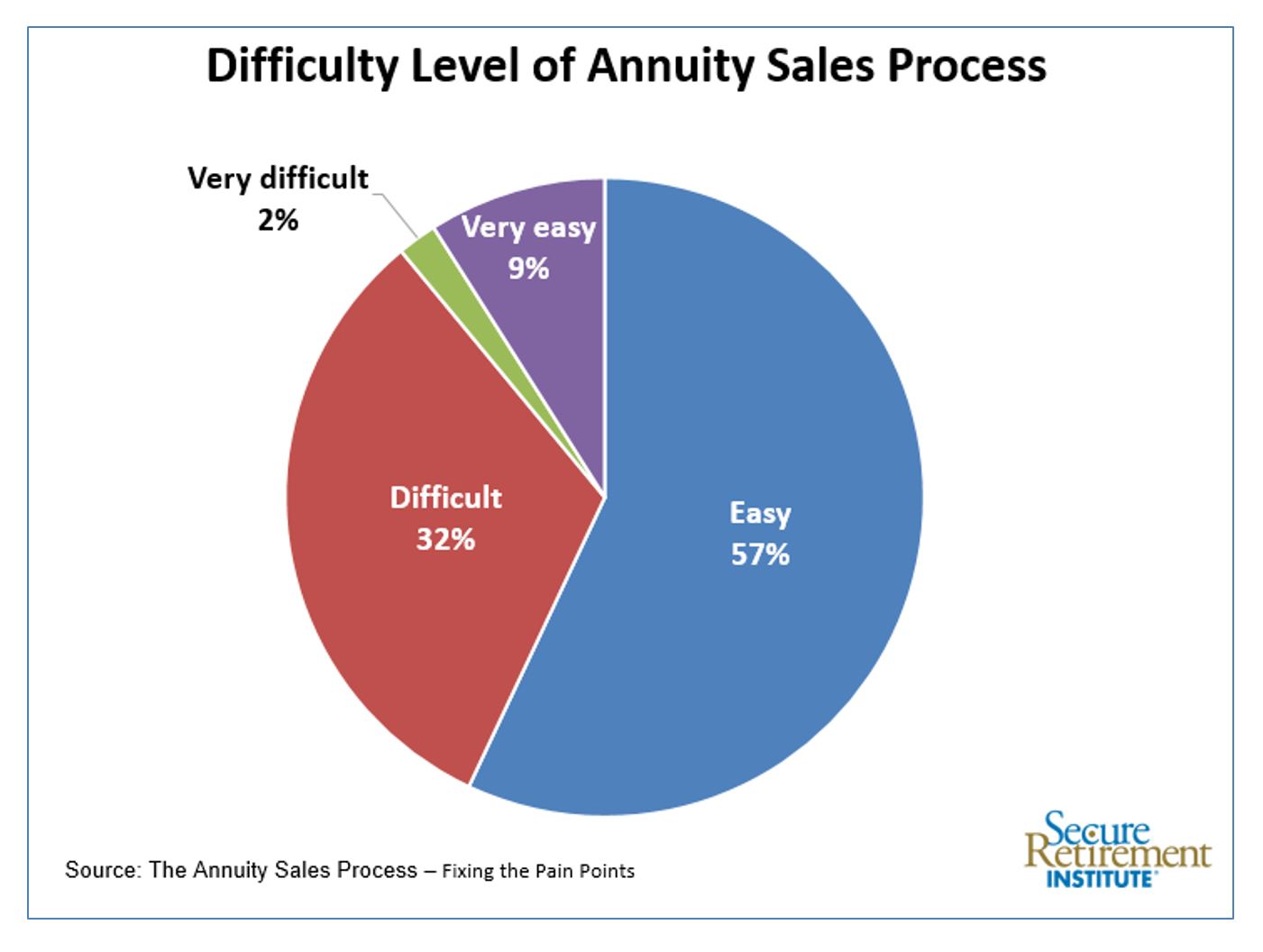

Compared with other investments, selling insurance products like annuities often requires a more extensive process. More than 6 in 10 advisors, however, describe the annuity sales process, from initial client discussions through transactions, to be “very easy” or “easy.”

While there were no clear differences in the assessment of the sales process across channel, more experienced advisors were more likely than less experienced advisors to consider the process to be easy, 69% of those with 20 or more years of experience versus 58% of those with two to four years of experience.

When asked why advisors found the process difficult, the top reasons given were that the annuity product designs are too complex (63%), the process requires extra sign-offs, paperwork and supervision compared with other products (63%), and a variation in procedures across carriers (32%).

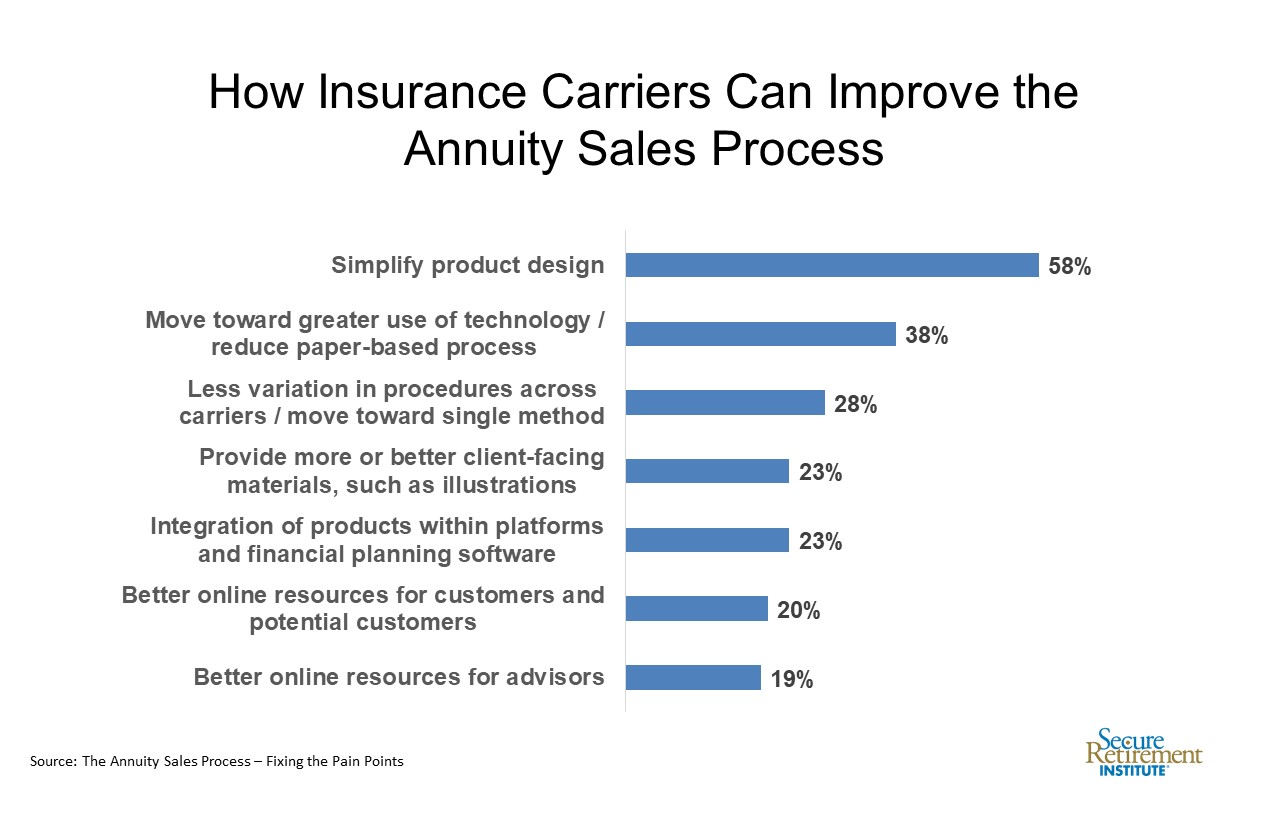

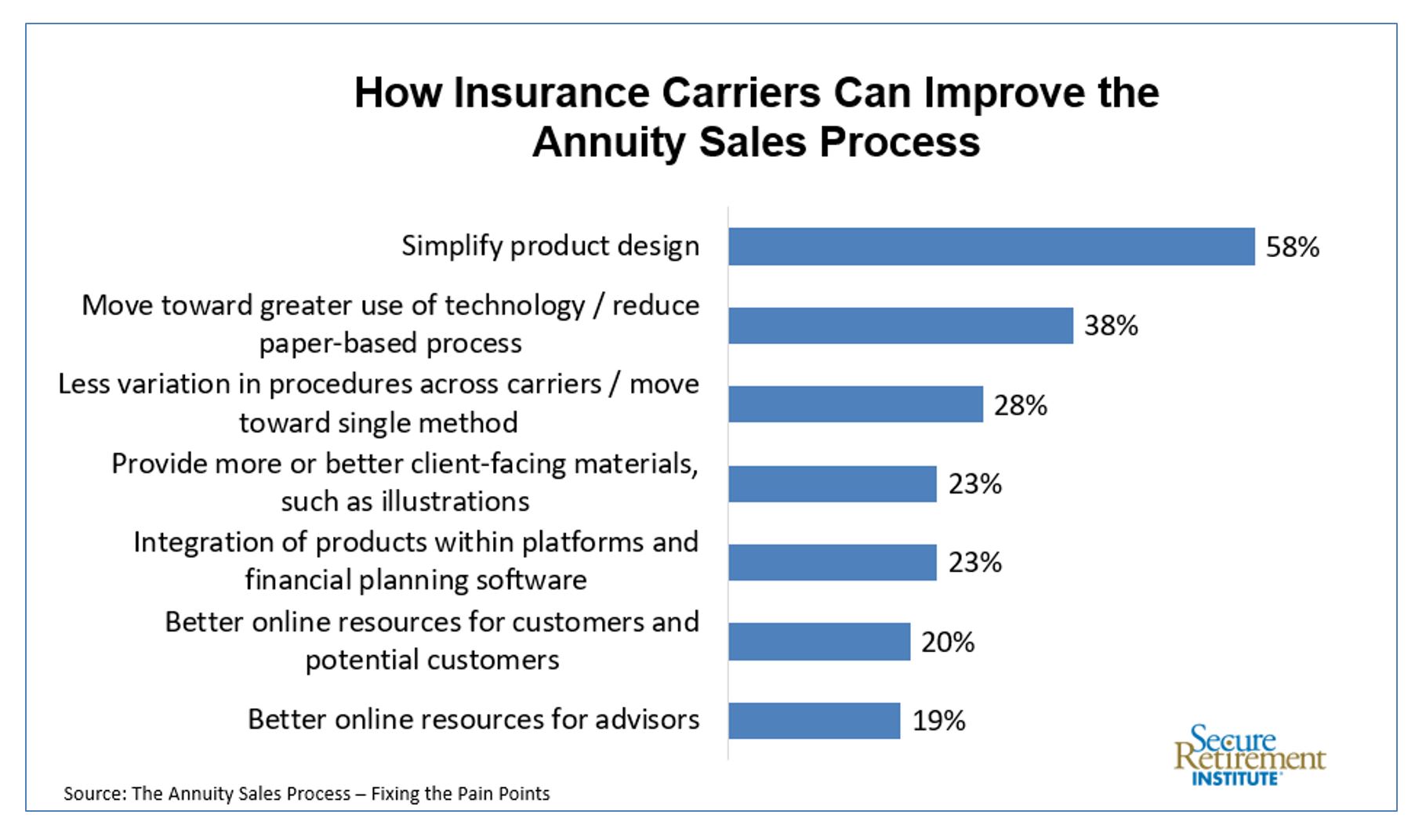

Although most advisors do not perceive the sales process to be difficult, there is always room for improvement. The top recommendations to carriers all involved simplification and efficiency: making designs less complex; moving toward greater use of technology and reducing paper-based processes; and reducing variation in procedures across carriers.

Making the annuity sales process simpler is especially important since other SRI research shows that when it comes to financial concerns, 57% of American workers are at least somewhat concerned about outliving their assets in retirement.

“To remain successful in an ever-changing competitive market, companies should continually evaluate the extent to which their products meet advisors’ preferences. Alignment with advisors’ preferences will ultimately lead to more sales, thereby improving the financial security of more Americans,” says Matthew Drinkwater, corporate vice president, Retirement Research, SRI.