As the pandemic spread, images of nursing homes and assisted care facilities flooded the media. The sick and elderly were particularly vulnerable to this deadly virus and so many families were cut off from their parents and grandparents in the hopes of protecting them from exposure to COVID-19.

With this in mind, LIMRA surveyed more than 2,000 Americans to determine if the pandemic has shifted their thoughts about long-term care and insurance.

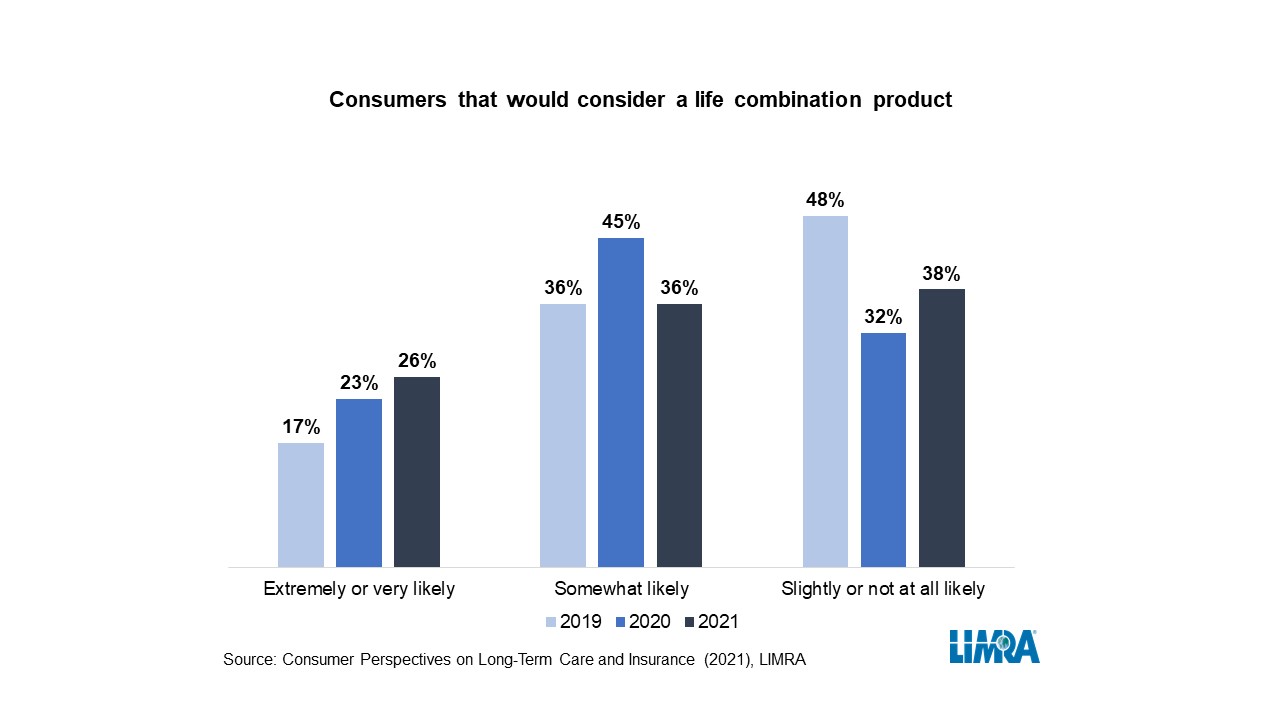

In January 2021, more than a quarter of Americans (26%) said it was very likely they would consider a life combination product (a life insurance policy with a long-term care (LTC) insurance component) if they were shopping for life insurance. This is 50% higher than in 2019. Overall 6 in 10 consumers said it is at least somewhat likely they would consider a life combination product if shopping for life insurance.

While Millennials expressed the most interest in life combination products — 35% said it was extremely likely they would consider life combination products — Baby Boomers are decidedly less enthusiastic. Just 17% say it was extremely likely they would consider these products and nearly a third said it was not likely at all.

“Baby Boomers, who are approaching or in retirement, may not feel the need for life insurance or may mistakenly believe Medicare will cover LTC expenses,” said Karen Terry, senior research director. “Younger individuals, however, may find life combination products appealing because they mitigate the financial risk of dying unexpectedly and the costs of long-term care.”

The top five reasons people give for considering a combination life insurance product include:

- Concern that LTC costs may deplete or exceed my savings – 35%

- It is a more economical use of my current assets – 33%

- Benefits will be paid even if I don’t incur LTC expenses – 29%

- LTC insurance (on its own) is too expensive – 26%

- I can't afford two separate (life and LTC) policies – 25%

The study found consumers facing high levels of stress as caregivers for adult relatives and/or children showed the greatest interest in life combination products. More than a third (36%) of caregivers with high stress levels said they were very likely to consider buying a life combination product, compared with just 21% of those who said they had low stress levels.

“These consumers recognize better than anyone the demands of providing care for aging parents or other relatives with declining health,” noted Terry. “Their experiences as caregivers make life combination products, which offer financial protection against their own long-term care needs, that much more attractive.”

Consumers are attracted to life combinations products for a number of reasons. From a product design standpoint, consumers place the greatest value on having the option to receive care at home or a facility. The study found 6 in 10 consumers would prefer to receive long-term care at home (unconditionally or until they have to move to a facility). This preference increases among older consumers.

Life combination products offer consumers the ability to address multiple financial risks they face as they age. According to the U.S. Department of Health and Human Services, someone turning 65 today has almost a 70% chance of needing some type of LTC services and support in their remaining years1. Life combination products can cover the costs of LTC so that a family’s savings and financial security are not put in jeopardy. It’s just another way life insurance protects a family’s financial future.

LIMRA is honored to lead the Help Protect Our Families campaign, an industrywide effort to raise awareness about the importance of life insurance and help carriers and distributors address the growing coverage gap in the United States.

1LongTermCare.gov