For decades, Americans have saved in workplace and individual retirement accounts (IRAs) on a tax-deferred basis. Workers gain access to their retirement savings when they change jobs or retire. In almost all cases, workers can cash out their accumulated balances immediately, or wait until they reach retirement to cash out.

Every year, defined contribution (DC) plan participants roll over more than $500 billion into IRAs after they retire or change jobs. Secure Retirement Institute® (SRI®) predicts this to exceed $760 billion within the next five years.

SRI research estimates that IRA rollovers represented approximately $565 billion in 2019, and jumped to $623 billion in 2020 as pandemic-related disruption led to an increase in the number of people leaving their employers. Driven largely by the accrual of balances in workplace savings plans, rollovers rank among the largest financial transactions Americans will make.

SRI’s recent Money in Motion: Understanding the Dynamics of the IRA Rollover Market study shows 6 in 10 investors (ages 40 to 75) who recently left an employer decided to roll a DC plan balance to an IRA. The study looked at what drives investors to rollover money (or keep it in their current plan), when they make these decisions, and who helps influence these decisions.

When Investors Decide to Roll

Deciding to roll a balance from a DC plan to an IRA is a complex decision. Both recent retirees and those who voluntarily changed jobs (or were recently laid off) face distinct challenges.

Most investors (54%) decided to roll a retirement plan balance prior to leaving their former job. Further, more than half of those investors, and 32% of all respondents who completed a rollover, decided to so 90 or more days before leaving their job or retiring.

Those conducting rollovers with larger balances were more deliberate, with 68% of those who rolled a balance of $500,000 deciding to do so before they left their former employers, and 57% decided to do so 90 or more days prior to leaving their job. Comparatively, only 39% of those who rolled a balance between $5,000 and $25,000 decided to do so prior to leaving their former employer.

Investors Value Professional Advice

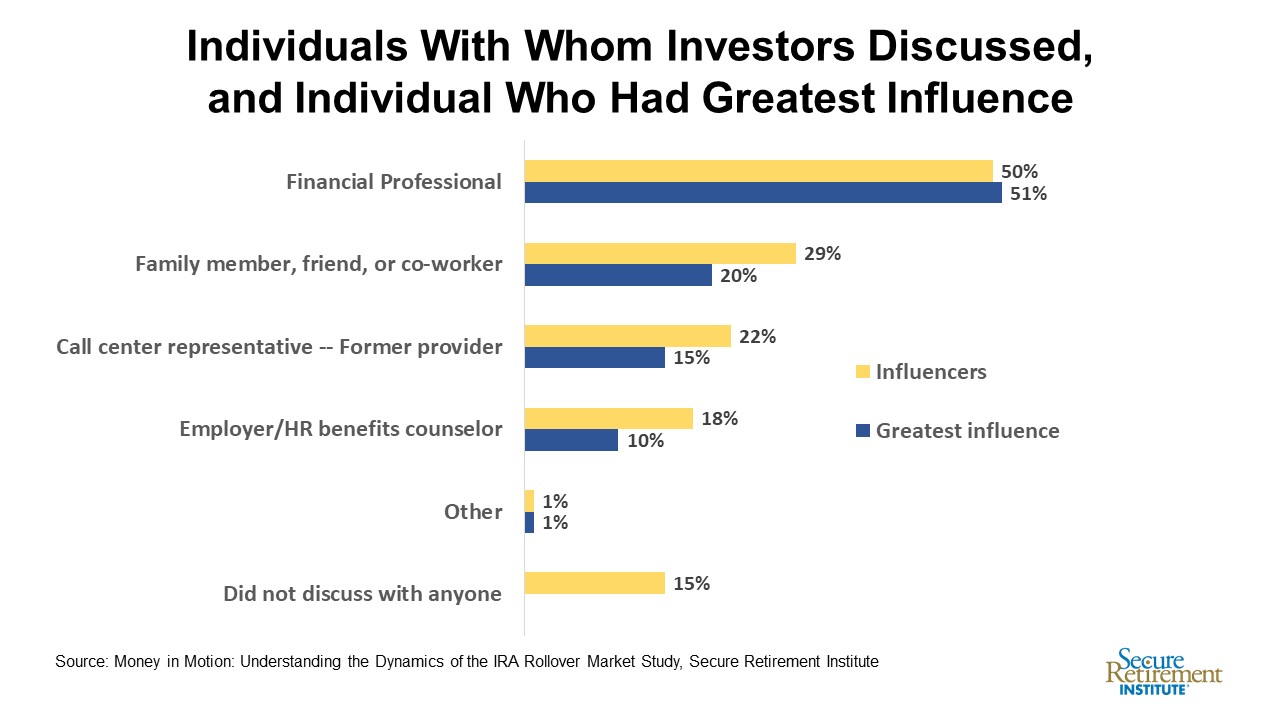

More than 8 in 10 (84%) investors who complete a rollover discussed their decision with someone before taking action. Fifty percent of investors spoke with a financial professional before rolling a balance, and 51% said that a financial professional had the greatest influence over their decision to do so. Older individuals (between 65 and 75) were even more likely to consult with a financial professional, with 56% of respondents having done so prior to rolling a balance and the majority citing their financial professional as the most influential person with whom they spoke.

Convenience Drives Investors to Stay

One quarter of investors who left an employer within the past two years left the entire balance in the DC plan. Investors decide to leave their money in the DC plan for a number of reasons.

The top five are:

- Convenience;

- No decisions had yet been made;

- Investment performance has been good within the plan;

- They did not currently need the money; and

- The former plan has provided good service.

The study found that compared with those who chose to roll the money, those who kept their money in their former employer’s DC plan are more likely to be younger; be women; have worked at an educational institution, hospital/healthcare organization, or government employer; or have worked at an employer with 5,000 or more employees.

Only 3% of investors who left an employer within the past two years elected to convert their balance into an annuity, possibly reflecting the low availability of this payout option — only 28% of these investors had an annuity payout option.

“Twenty-six percent of investors who left an employer within the past two years took no action with their money, keeping the entire balance in the DC plan. These accounts represent future money in motion, as investors may decide to cash out, roll over, transfer, or begin taking income from the account at any point,” said Drew Maresca, research director, Retirement Research.