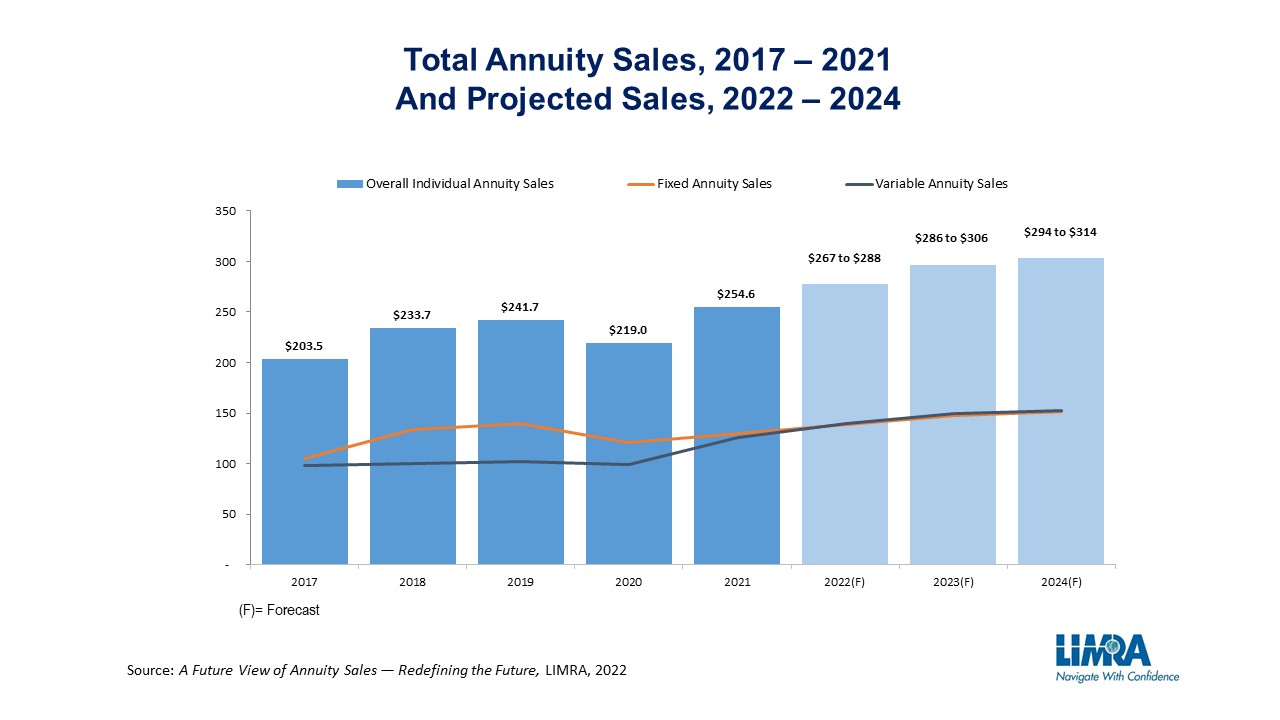

Despite the continued challenges resulting from the COVID-19 pandemic, the annuity industry rebounded strongly — with first quarter 2022 seeing total U.S. annuity sales increase 4% to $63.3 billion. LIMRA expects this momentum to continue through the next several years.

“The outlook for rising interest rates and fairly level equity markets will have investors continuing to look for the balance between protection, growth, and guaranteed income, creating a strong potential for individual annuity sales to break the all-time record levels of sales experienced in 2008,” says Todd Giesing, assistant vice president, LIMRA Annuity Research.

Although there are many variables to consider, including inflation, technology implementation, the regulatory environment and low interest rates, LIMRA expects economic conditions will continue to improve, particularly rising interest rates, allowing manufacturers the ability to add more value to their solutions.

“We see steady growth in both fixed and deferred annuity sales with the potential for seeing over $300 billion in sales in just two short years,” Giesing says.

A Growing Market

According to Oxford Economics, the U.S. population aged 65 or over is expected to grow by more than 8.5 million by 2026. The aging of the U.S. population creates a favorable environment for the sale of individual annuities, since LIMRA data show individual annuity product sales mainly cluster around the traditional retirement age of 65.

Giesing notes, “We saw a massive amount of unemployment in the U.S. due to COVID-19 events, resulting in a portion of Americans near retirement altering their initial plans and retiring earlier than anticipated.”

When it comes to the traditional variable annuity (VA) market, it rebounded strongly in 2021, with sales increasing 16% from the prior year. A significant amount of the growth in 2021 was driven by products without guaranteed living benefits (GLBs), with sales in this segment growing 28%.

“By 2023, traditional VA sales will flatten out as economic conditions continue to improve. There will be continued pressure not only on investment-focused traditional VAs, but also on traditional VAs with guaranteed living benefits from carriers that have shifted their focus to registered index-linked annuities, or RILAs,” Giesing says.

In fact, RILA sales experienced a staggering 62% growth in 2021 as investors increasingly looked for safety. This increase in the inventory of market offerings continued throughout 2021, including the increase of RILA product offerings with guaranteed living benefits. Improving economic conditions will help spur RILA growth along with the continued focus and new entrants and products entering this market.

“After the challenges faced during the height of the pandemic, the indexed annuity market rebounded with 2021 sales increasing 15%. Similar to the traditional VA market, sales of products without guaranteed living benefits grew at a faster clip as investors were looking for the balance of principal protection and growth,” Giesing notes.

As June marks Annuity Awareness Month, it’s a good time to see where the annuity market is going and how it can play an important role in financial security during retirement. The annuity market offers a variety of products with different protections and features designed to meet consumers’ specific financial needs.