Even before the COVID-19 pandemic, unpaid caregivers struggled with the demands of work and saving for the future. The pandemic brought on additional work/life disruptions with stay-at-home orders, school closures, and reduced ability to outsource caregiving. The challenges also affect workers’ future retirement security since retirement income is often dependent on one’s ability to work and, through that work, accumulate savings.

A new Secure Retirement Institute® (SRI®) study, Staying the Course: Navigating Unpaid Caregiving Obstacles to Retirement Security, explored the impact of caregiving on workers’ retirement savings, as well as the actions and employer benefits that may help caregivers plan for a secure retirement.

The research found that among those who experienced an employment gap due to unpaid caregiving, only 55% of women took action to compensate for lost retirement savings due to this leave, compared to 86% of men.

“As women return to the workforce post-pandemic, steps large and small to boost savings — such as ensuring they are contributing enough to meet the employer match, increasing savings rates, or making catch-up contributions if their age permits — can help improve their retirement preparedness,” said Cecilia Shiner, research project director, SRI.

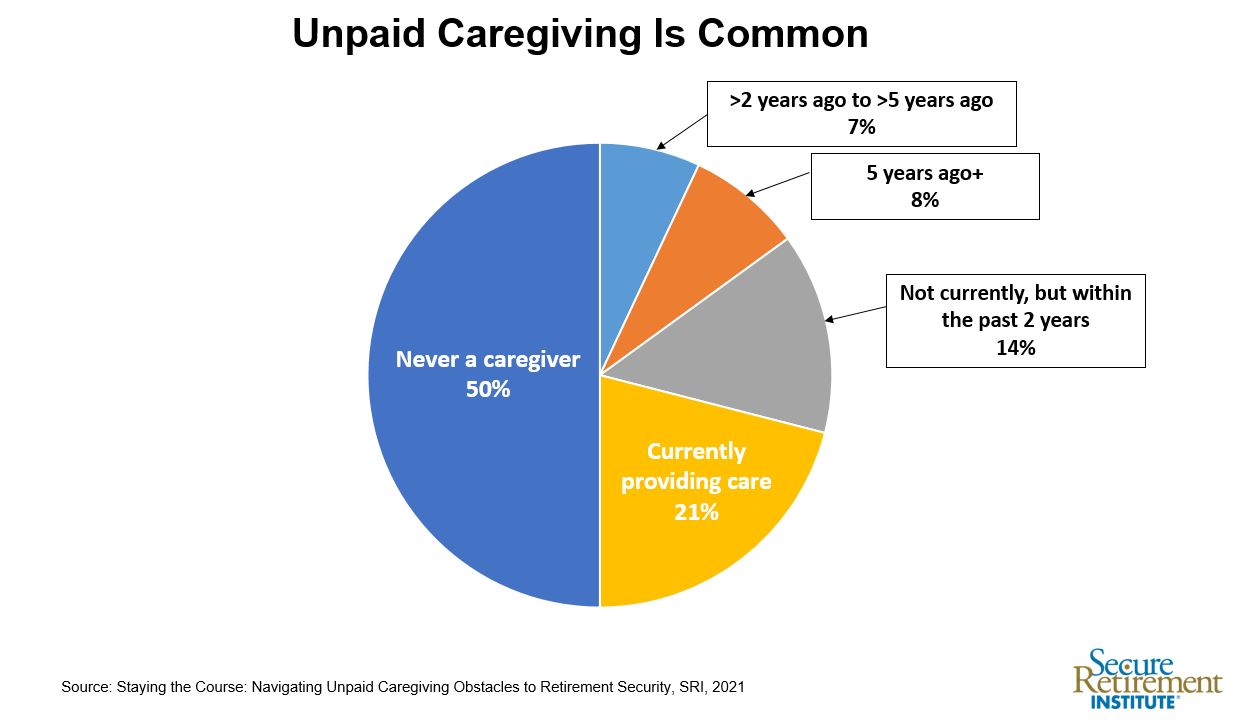

Unpaid Caregiving More and More Common

According to SRI research, 1 in 5 workers is currently an unpaid caregiver. Among the 35% of workers who have provided care in the past two years, 43% provided care to children under the age of 18. However, nearly 1 in 5 workers (18%) provided care to both children and adults in the past two years.

Nearly half of workers who have been unpaid caregivers had their paid work impacted (i.e., taking an unpaid leave of absence, turning down a promotion, or reducing their hours).

Undermining Financial Security

Unpaid caregiving can have a negative impact on savings and retirement readiness. Caregivers report needing to withdraw money from a retirement account for non-retirement purposes (13%), stop saving for retirement (12%) and delaying retirement or determining they can never retire (10%).

Caregiving-driven employment gaps can weigh on the minds of workers. Half of caregivers who have interrupted their employment in order to provide unpaid care are worried about the impact work disruptions may have on their retirement security. In fact, 1 in 5 strongly agree that such interruptions will undermine their security in retirement.

The financial impact of unpaid caregiving not only affects retirement readiness but also can undermine their current financial security. One in five unpaid caregivers reported taking on more debt (21%), spending their existing emergency savings (21%), and halting saving for future emergencies (17%).

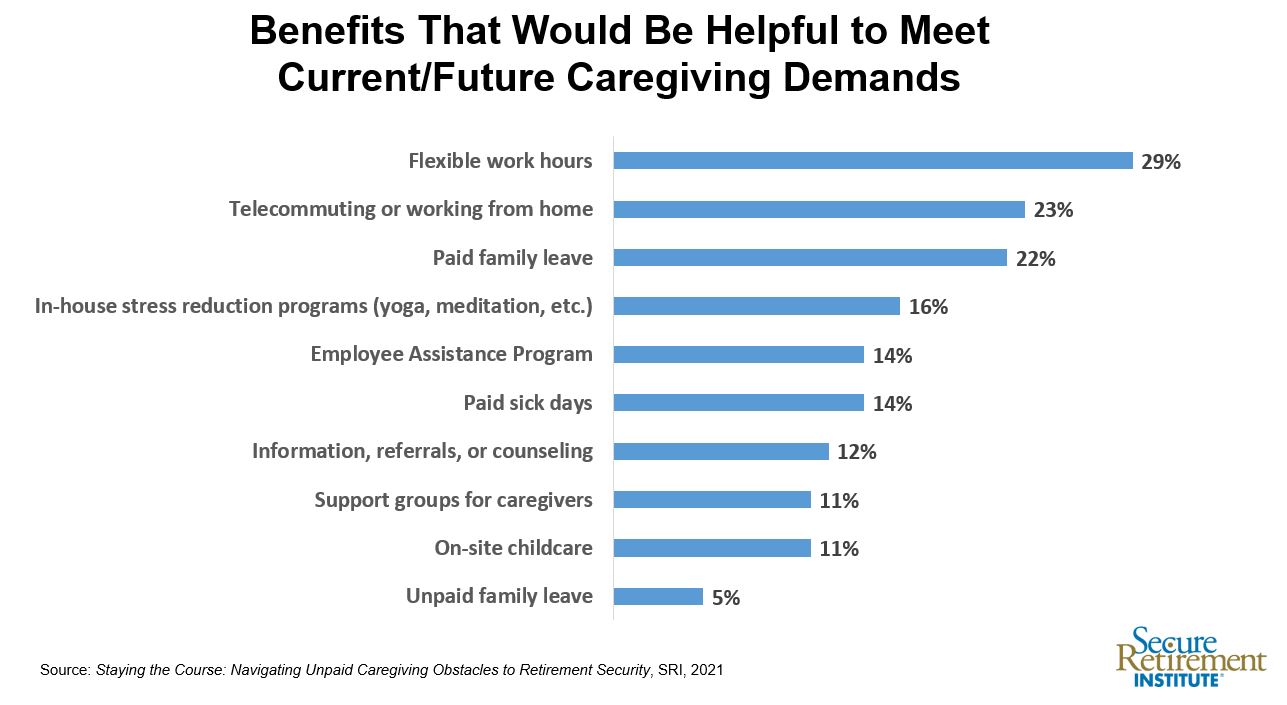

Employer Benefits Are Critical

While most benefits are not designed to meet the needs of unpaid caregiving, many of them can help with those demands. Benefits that offer workers the flexibility to meet their caregiving responsibilities, such as paid family leave, flexible work hours, and telecommuting/work-from-home are among the benefits caregivers say they value.

More than 60% of unpaid caregivers with benefits (such as on-site childcare, caregiving support groups, information, referrals, and counseling to help caregivers) feel that their employers support their caregiving challenges, compared with a quarter of those without available caregiving benefits.

Unpaid caregiving can present a great challenge for workers, but support from employers and plan providers can make a difference. Below are three ways employers and plan providers can help unpaid caregivers manage competing demands on their time and energy, and avoid negative financial impacts of unpaid caregiving.

- Provide flexibility: As part of their benefits package, offering flexible work schedules and paid time off can allow unpaid caregivers to maintain their income while being a caregiver and, in turn, allow them to continue to save for retirement.

- Enhance communications: Plan providers can play a critical role in helping their clients support unpaid workers’ retirement readiness. As workers return to the workforce post-pandemic, plan providers can enhance participant communications to help them boost their retirement savings (such as ensuring they are contributing enough to meet the employer match, increasing savings rates, or making catch-up contributions if their age permits).

- Add an emergency savings plan: Employers can work with their plan providers to offer workplace emergency saving accounts to their retirement savings plans to help build workers’ safety net.