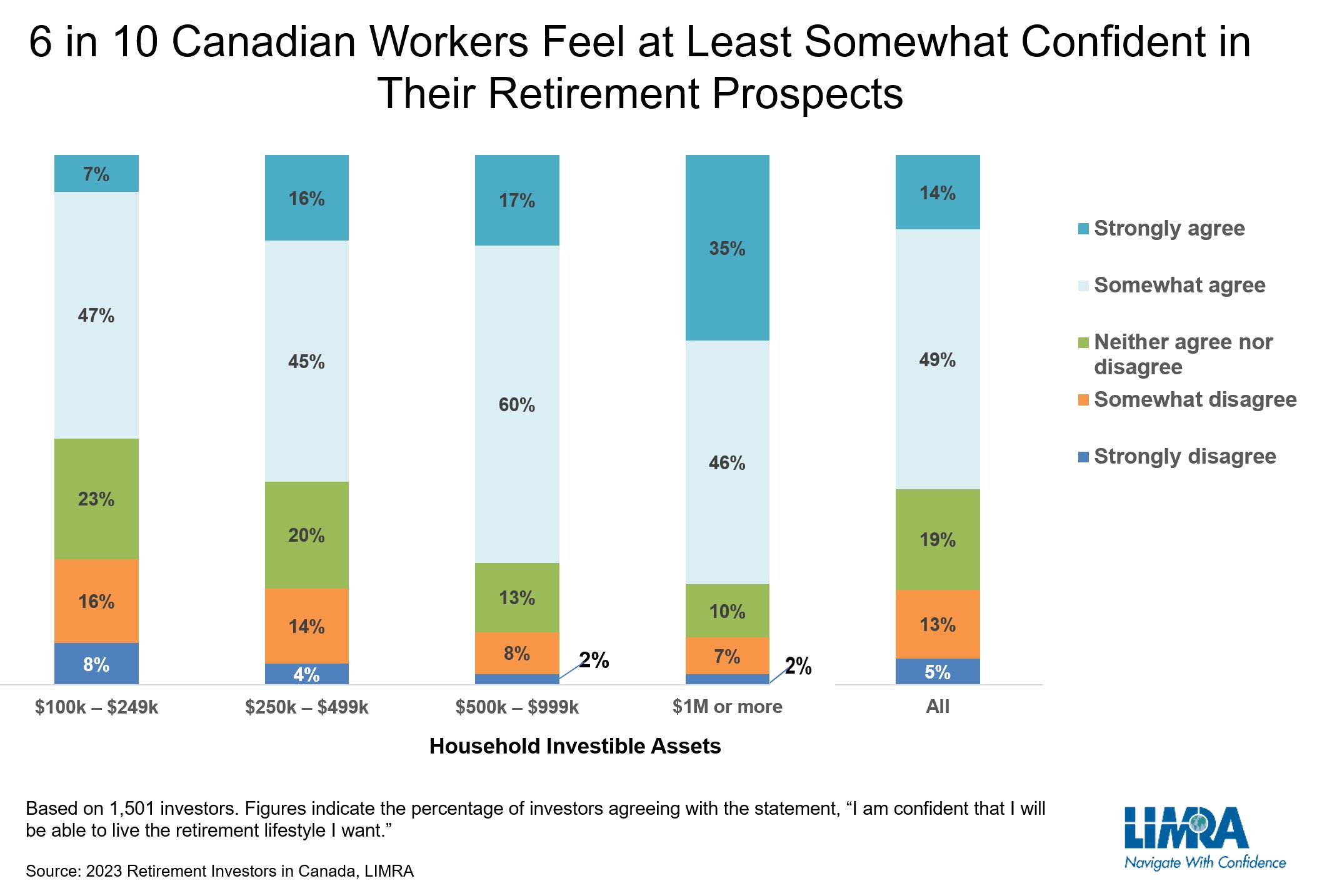

According to a recent LIMRA survey of retirement investors in Canada, nearly 2 in 3 investors feel confident that they will be able to live the lifestyle they want in retirement. LIMRA’s Canadian Retirement Investors study looked at retirees and workers aged 40 to 85 years old with at least $100,000 in household investable assets.

Different wealth segments have widely differing levels of confidence in their ability to live the kind retirement lifestyle that they are looking forward to experiencing. Nevertheless, retirement confidence should not be solely determined by wealth; even investors with substantial savings need to do in-depth planning and skillfully deploy their assets to meet their lifestyle goals. A strong predictor of confidence is the presence of a plan to manage income, expenses, and assets throughout retirement. Formal written plans, often developed with the assistance of a financial professional, are especially important because they provide the best sense of what risks will be in retirement.

Those without sufficient lifetime-guaranteed income from traditional government or private pensions, other sources will have to cover basic living expenses through non-guaranteed sources, potentially putting these future retirees at greater risk of a reduced standard of living. Investors across wealth segments overwhelmingly agree that lifetime-guaranteed income is important for retirees’ peace of mind. However, LIMRA’s study finds only 3 in 10 investors would be willing to annuitize some of their assets in retirement. The annuitization concept is more popular among younger investors and those with higher household incomes.

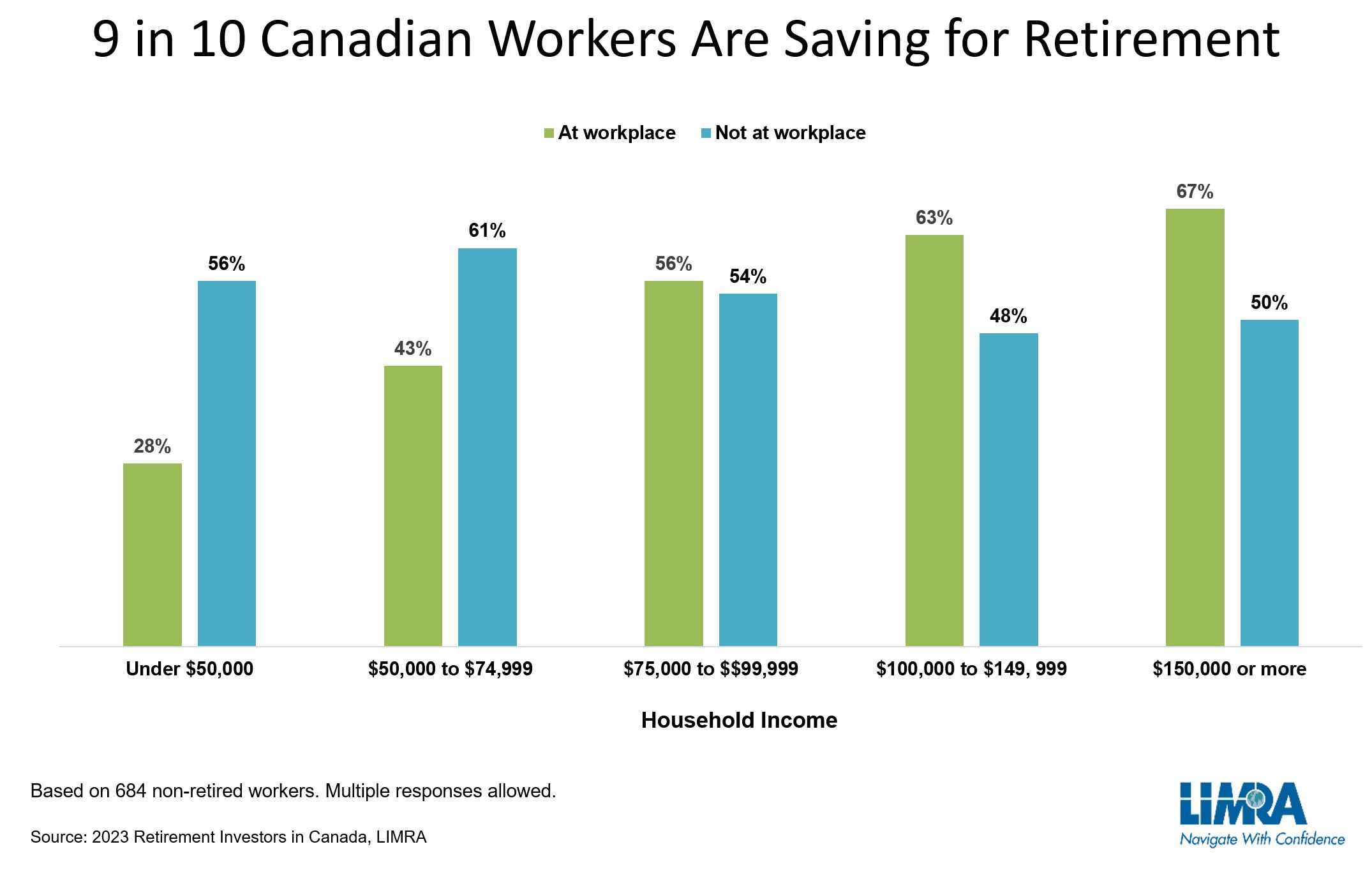

Most Canadians Are Saving for Retirement

According to LIMRA’s study, the vast majority (91%) of Canadian workers are saving for retirement, either at their workplaces or elsewhere (or both). As expected, saving at the workplace increases as household income increases. Higher-income workers are more likely to work at employers offering defined contribution (DC) plans, and they are in a better position to put aside money each paycheck, compared with lower-income workers.

More than two thirds (69%) of workers said they were confident they were saving enough for retirement. Men, those who work with financial professionals, those who own annuities, and those who have higher self-rated investment and financial product knowledge tend to have greater confidence.

Having a formal written plan is also strongly linked to confidence: While 86% of those with a formal written plan are “very” or “somewhat” confident that they are saving enough, less than 6 in 10 (58%) of those with no retirement plan express the same level of confidence.

Plans for retirement must address longevity risk and consider both the likelihood and impact a very long retirement could have. While the majority of non-retired Canadian workers feel confident they will be able to live the lifestyle that they want in retirement, carriers and advisors should stress the importance of lifetime-guaranteed options and how a formal written plan can help them ensure they are able to live the retirement they hope for.