Media Contacts

Catherine Theroux

Director, Public Relations

Work Phone: (860) 285-7787

Mobile Phone: (703) 447-3257

8/28/2025

Each day, more than 11,000 Americans turn 65, and a majority (56%) of them will need some level of long-term care (LTC) services within their lifetime, according to the Department of Health and Human Services (HHS). Yet, LIMRA estimates just 3% of Americans over age 50 have any LTC insurance protection, leaving many people on the financial hook to cover these expenses on their own.

There has been considerable discussion about the U.S. aging population regarding retirement savings and the need to secure guaranteed retirement income. Yet Americans also face another substantial financial risk — needing and affording LTC services. According to HHS, the need for LTC services will be substantial for those ages 65 and over:

The costs of LTC services are high and continue to rise. The annual median cost of home health aid exceeds $77,000, and the median yearly cost for a semi-private or private room in a nursing home is between $111,000 and $127,000, depending on the state/location.

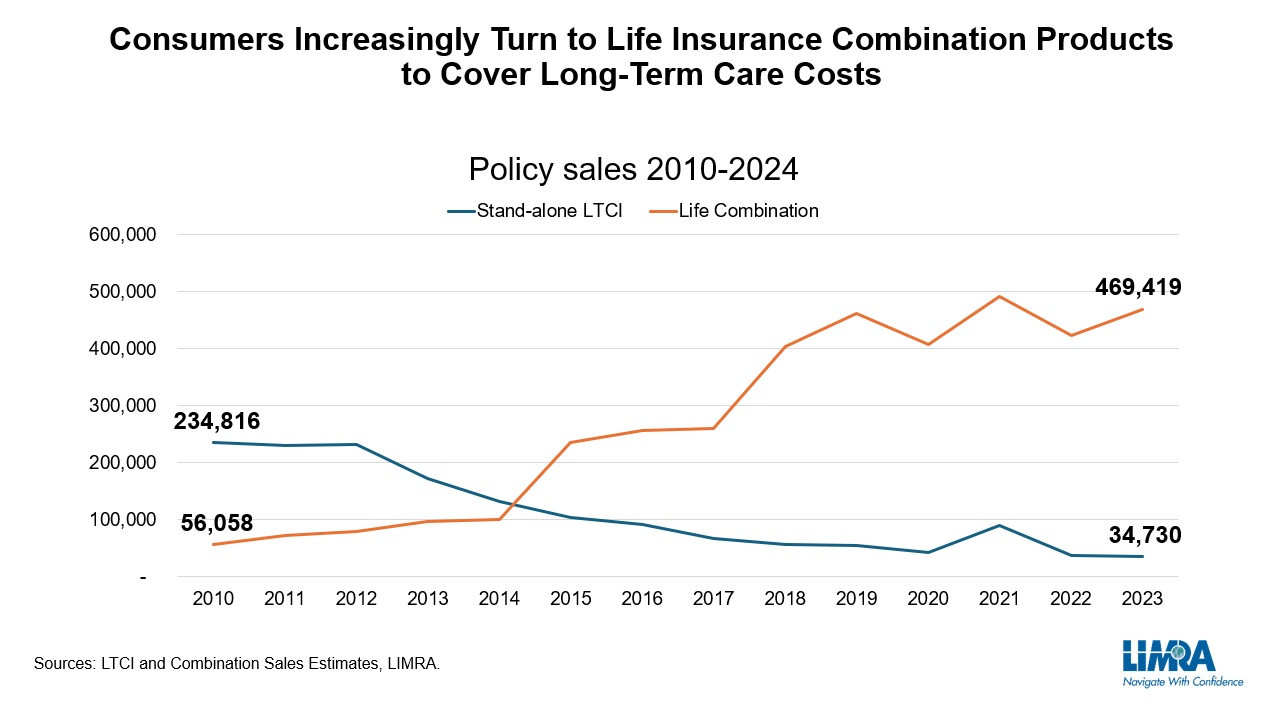

How the LTCI market has evolved

The entire LTCI market has experienced considerable changes over the past 15 years. As LTC costs jumped beyond projections and policy rate hikes to mitigate those costs dampened future sales, more than three-quarters of stand-alone LTCI carriers left the market by 2012. However, the need for protection persisted, driving growth in the combination life/LTCI market as new companies entered the market, introducing new products and adapting existing product design to make it more accessible to middle-income and mass affluent consumers.

“Today, there is a full suite of products from those with chronic illness riders all the way through to the traditional stand-alone LTCI policy that's available to address different people's needs,” said Karen Terry, corporate vice president and director of LIMRA Insurance Research. “While the rise in combination products has been steady, we also have witnessed changes in the stand-alone market that address the issues that led to the significant premium increases of the past.”

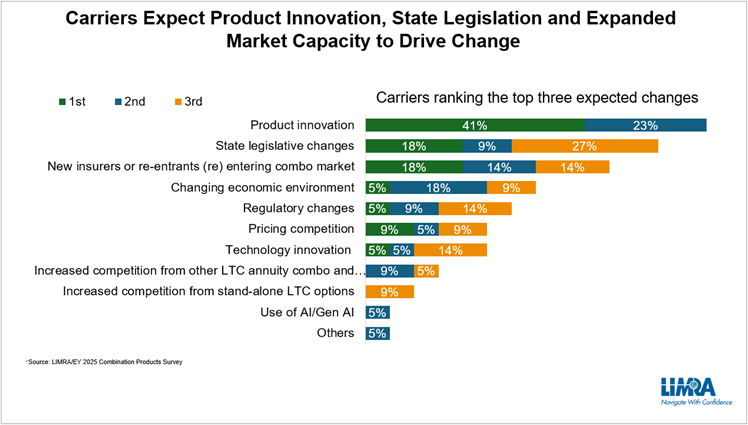

Carriers Look to Product Innovation to Spur Market Growth

In a new study, conducted jointly by LIMRA and EY, 4 in 10 carriers surveyed said they expected product innovation to be the number one driver of growth in the coming years. Although comprehensive product innovation is rare, expansions in workplace products are likely. LIMRA has noted that companies have already begun to enhance their products with caregiver resources and wellness programs.

The study found carriers offering combination products — perhaps stung by their experiences in the stand-alone market — are most concerned about actuarial modeling/valuation and pricing, and assumption setting. Today, there isn’t a lot of claims data yet to analyze. Carriers are mindful that getting the pricing and actuarial assumptions right will have long-term effects on their sustainability and reputation in the market.

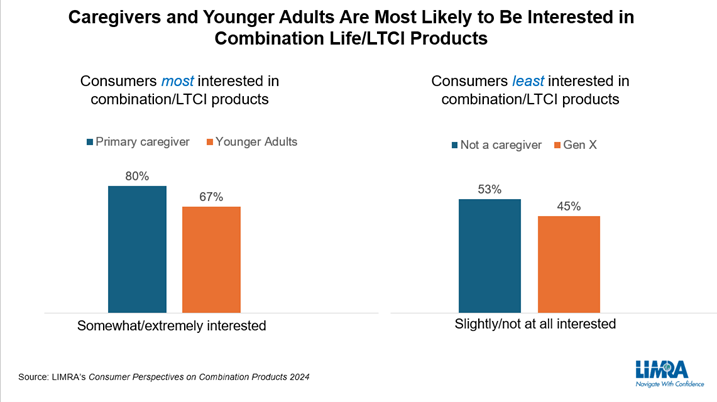

An Unexpected Audience for Combination Products Emerges

There is an indirect cost to families dealing with LTC needs. LIMRA research has shown that caregiving often falls to the family. LIMRA research shows the stress and impact of caregiving has created an unexpected audience for LTCI solutions, particularly in combination products. According to a recent survey, younger generations and primary caregivers express more interest in combination life/LTCI products.

“Our research suggests that those in the sandwich generation — specifically Millennials — who are caring for aging parents and younger children are very open to combination products,” said Bryan Hodgens, senior vice president and head of LIMRA Research. “While stand-alone products typically attracted an older customer, combination products can expand the market to younger adults, potentially making coverage more affordable.”

More than 7 in 10 say being a caregiver has impacted how they think about their own future care needs. These consumers are more likely to want to proactively plan for their potential LTC needs and worry about becoming a burden on their loved ones. Consumers, in general, say they are attracted to the flexibility of the products and the peace of mind they get because they have financial protection should they need care.

To learn more about the combination life/LTCI market, watch the latest Industry Insights With Bryan Hodgens episode: Is Life Insurance the Answer to the Growing Long-Term Care Needs in the U.S.?

Director, Public Relations

Work Phone: (860) 285-7787

Mobile Phone: (703) 447-3257