Media Contacts

Helen Eng

LIMRA Retirement Public Relations/Social Media Lead

Work Phone: (860) 285-7834

5/20/2025

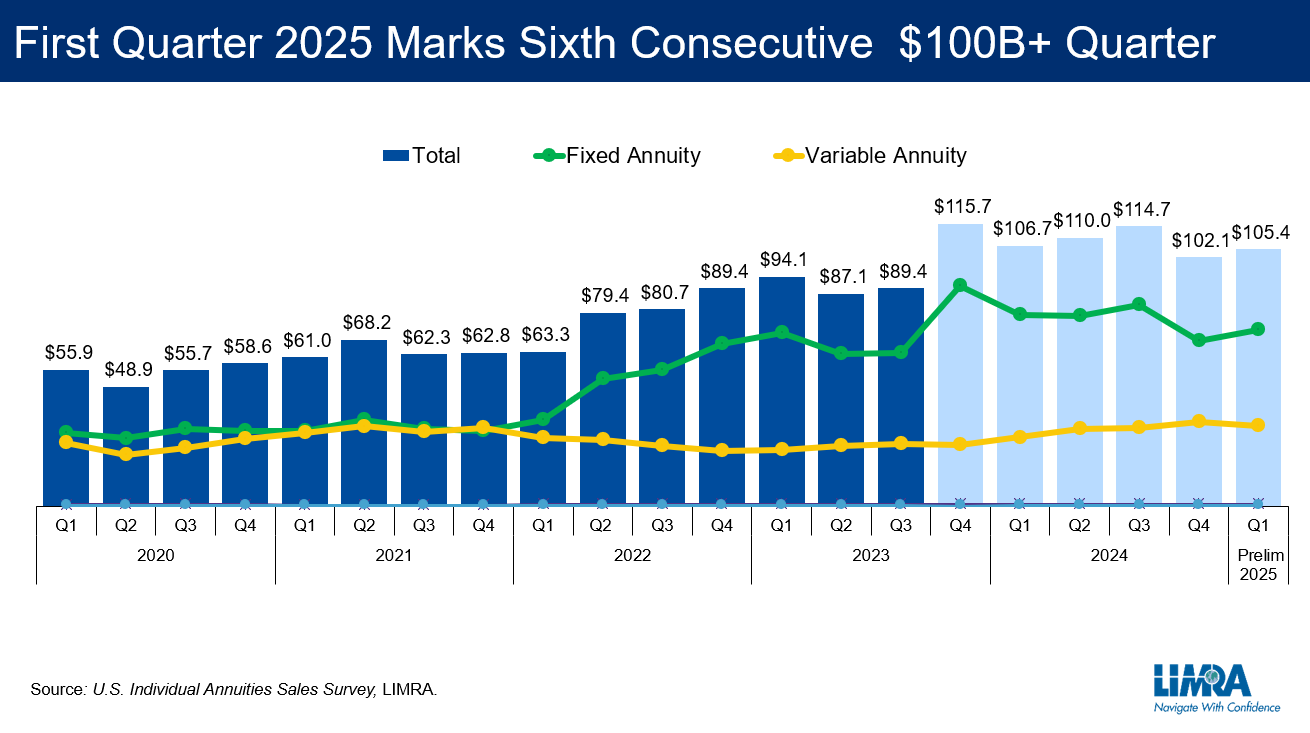

Coming off the third year of record-high annuity sales, total annuity sales were $105.4 billion in the first quarter of 2025 — just a bit lower (-1%) than the record set in first quarter 2024 but rebounding 3% from fourth quarter of last year. This is the sixth consecutive quarter of $100+ billion in sales. Slightly lower interest rates and a booming equity market resulted in double-digit growth in traditional VA and RILA product sales but declines in fixed annuity products.

“As market volatility increased throughout the quarter, our research showed consumers’ sentiment about the economy plunged. By the end of the quarter, 6 in 10 consumers said they were very concerned about the economy — a 14-point difference from January,” said Bryan Hodgens, senior vice president and head of LIMRA research. “As a result, consumers sought out investment protection and safety. Our data show March marked the second highest monthly sales in history and fixed-rate deferred product sales having the highest monthly results in over a year.”

Although the economic outlook for the rest of the year appears uncertain, there are significant tailwinds favoring the annuity market. LIMRA expects total annuity sales to exceed $400 billion in 2025.

Favorable Demographics and Growing Need

U.S. demographic trends favor our industry. Through 2029, more than 4 million people will turn 65 each year and a larger proportion of them will retire without a pension. In 2024, just half of pre-retirees believed they had enough guaranteed lifetime income sources to cover basic living expenses, down from 58% in 2017.

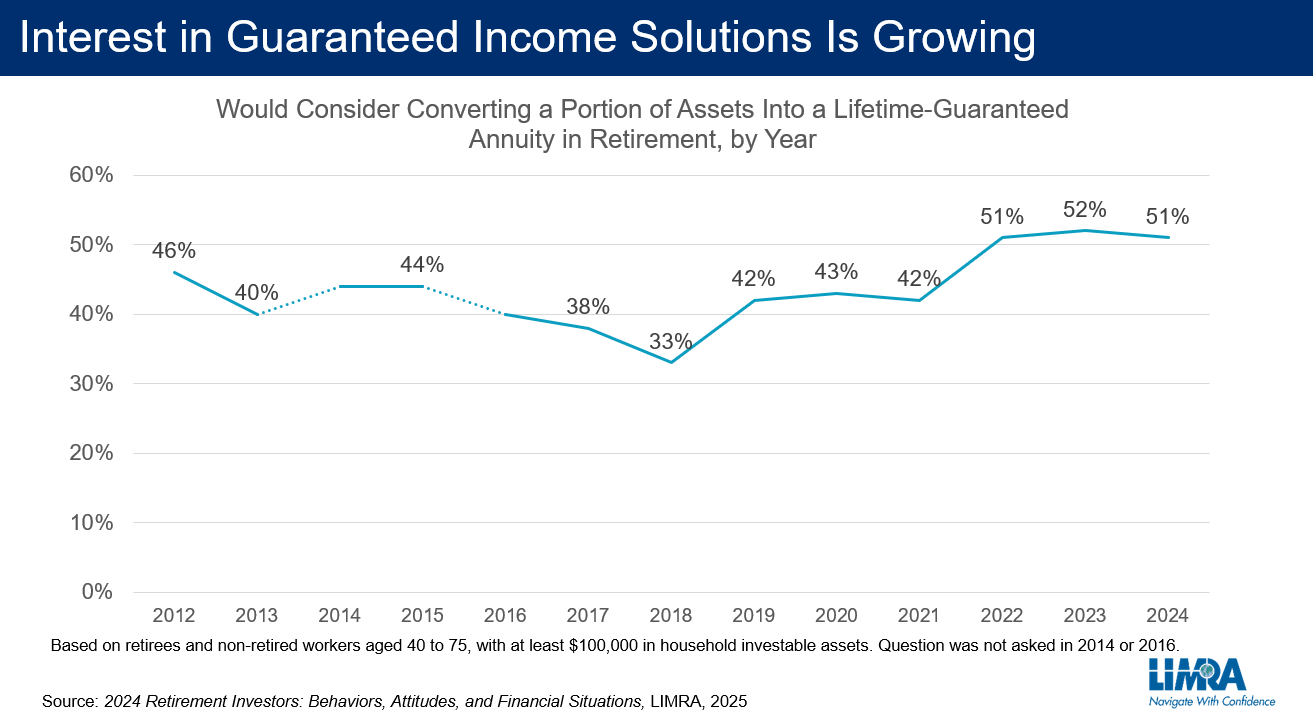

LIMRA research shows interest in converting a portion of assets to an annuity remains historically high, with over half of pre-retirees and retirees saying they would be interested.

Product Innovation to Address Investors’ Unique Priorities

Over the past decade, two products have evolved to become significant drivers of the sales growth. Registered index-linked annuities (RILAs) and fixed indexed annuities (FIAs) have grown from 23% of the $242 billion in total annuity sales in 2015 to representing 44% of the $434.1 billion in total sales in 2024.

The trajectory of the RILA market has been remarkable. Sales increased from $3.7 billion in 2015 to $65.4 billion in 2024 as the number carriers offering these products rose from 4 to 21. RILAs are attractive to both insurers and investors — providing investors the ability to mitigate equity market downturns and allowing companies greater flexibility to hedge against risk as market conditions change.

FIA sales too have witnessed tremendous growth as annuity carriers introduced custom indices, offered more flexible crediting methods, and improved and expanded income riders. Since 2015, FIA sales have increased more than 137% to $126.9 billion in 2024.

“With these indexed products, carriers have broadened their solutions across the risk spectrum to address investors’ individual needs,” said Hodgens. “For those investors most interested principal protection, fixed-rate deferred annuities offer safety and guaranteed return. As investors’ appetite for greater upside potential with limited market risk has grown, FIAs and RILAs are increasingly available, and our sales data suggest it is resonating with the market.”

Driving Distribution Expansion

Product innovation also plays a role to expand annuity distribution. While the industry adopts new technologies (artificial intelligence, data analytics, etc.) to streamline applications and claims processes and enhance lead generation, LIMRA also sees the industry focused on developing products designed to attract more registered investment advisor (RIA) interest.

“There is greater interest in balancing commission-based products and fee-based products. Today, just half of RIAs report selling annuities to their clients — the expansion of fee-based products may increase annuity sales through the RIA channel,” said Keith Golembiewski, assistant vice president and director of LIMRA Annuity Research. “As carriers incorporate advanced technology, they are able to sell both products side by side. Our research shows fee-based VAs and FIAs have doubled since 2020 to $7.7 billion in 2024.”

The contingent deferred annuity (CDA) market, while not entirely new, is growing and also designed to attract more RIAs. The product wraps an annuity on an advisory account, allowing an investor to create guaranteed income without relinquishing the assets. Since RIAs often are compensated with a percentage of assets under management, this may be an attractive new solution to create lifetime income for their clients.

Ultimately, there is $17 trillion in IRA assets on the table. The increased availability of capital through private equity investment and reinsurance, coupled with advanced technologies and product innovation, opens tremendous opportunity for the annuity industry.

To learn more about emerging trends in the U.S. annuity market, watch the latest Industry Insights With Bryan Hodgens episode: U.S. Annuity Market: New Opportunities Amid Economic Uncertainty.

LIMRA Retirement Public Relations/Social Media Lead

Work Phone: (860) 285-7834