LIMRA.com and LOMA.org will be off-line for scheduled maintenance August 8, 2026 from 8 a.m. - 12 p.m. ET.

Since the COVID-19 pandemic, the U.S. life insurance industry has seen remarkable growth, setting sales records for four of the past five years, including in 2025 where new annualized premium topped $17.5 billion. Policy sales also posted growth, jumping 7% in 2025.

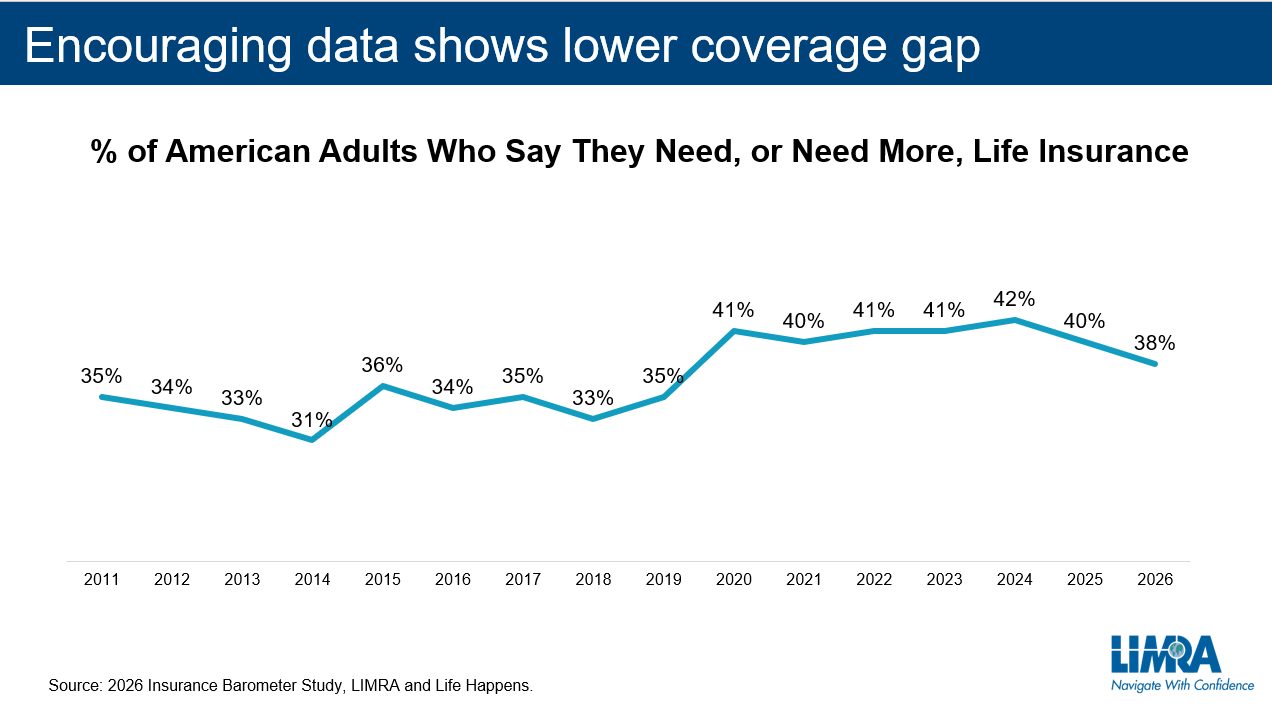

In conjunction with rising sales over the past five years, the Insurance Barometer Study, conducted annually by LIMRA and Life Happens, showed Americans’ increased awareness of their need for life insurance. Over the past two years, the coverage need gap has decreased, signaling people may be acting to get the coverage they knew they needed.

“Although the urgency associated with the pandemic has declined, the industry efforts to make the buying process easier and accessibility through technology has definitely had a positive impact,” said Steve Wood, research director, LIMRA Markets Research. “Today, an aging population and shifting distribution trends may prompt more insurers to integrate more wealth management, chronic illness and long-term care solutions into their life insurance products. Interestingly, new research shows these types of features are appealing to younger demographics as well.”

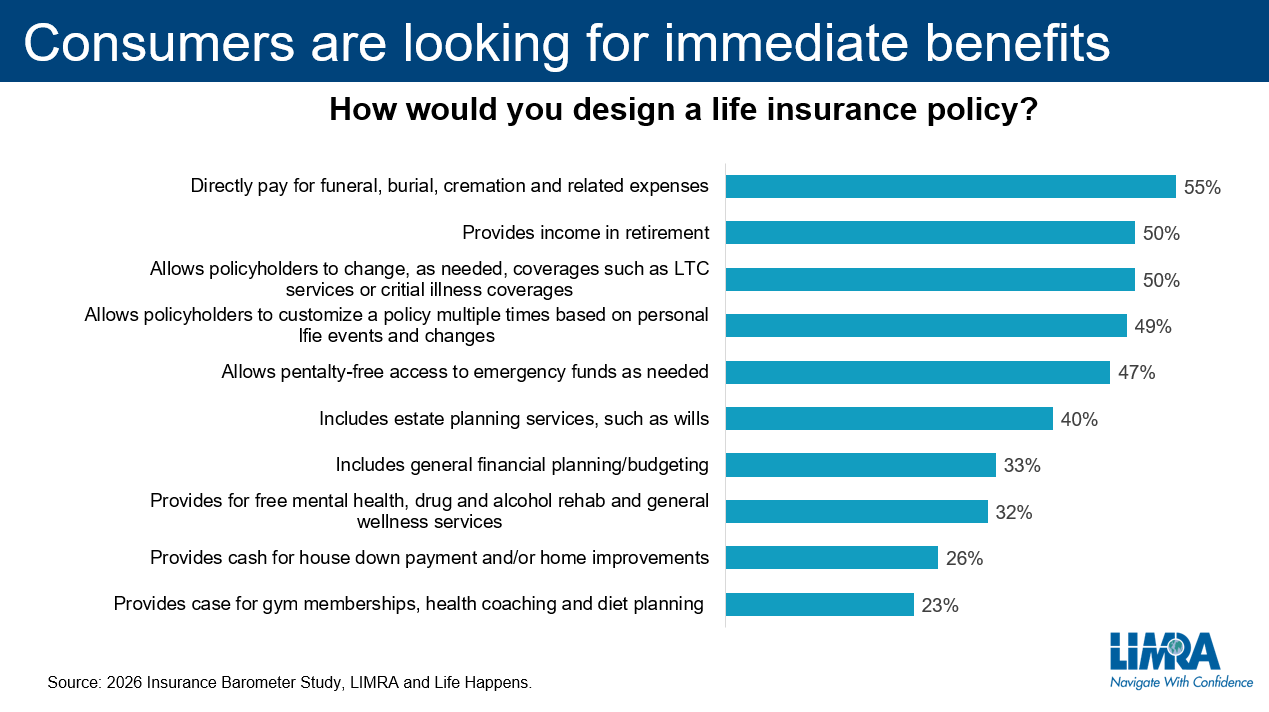

The 2026 Insurance Barometer study finds while a majority of people look to life insurance to cover burial and final expenses, it’s clear that many want the product to provide all sorts of living benefits and retirement income.

The study shows half of consumers would be interested in a policy that could create retirement income, would pay for long-term care services, cover critical illness costs or provide funds to cover emergencies. Half also noted they ideally would like a policy that could be customized multiple times, based on personal life events and changes.

“The reality is many of these wish-list items are already available. People can convert their cash-value life insurance into retirement income. There are products and riders that can cover costs of long-term care services, and life insurers have always allowed policyholders the ability to take loans from the cash-value of their policies to pay for school, emergencies, home loans, etc.” said Bryan Hodgens, senior vice president and head of LIMRA Research. “This suggests there is an opening to better communicate the broad ways life insurance can support holistic financial security and we are seeing life insurers rise to the occasion.”

Life insurers are working to improve access and understanding of life insurance by leveraging new technologies to make advisors’ jobs easier: simplifying products, streamlining digital processes and improving speed from application to decision to policy issue. This frees up advisors’ time navigating operational complexity to dedicating more time to educating their clients.

Life insurers are also building effective tools and seamless experiences so advisors can reframe life insurance away from outdated perceptions that life insurance is just about a death benefit to focusing on the living benefits the products offer that can address the top financial priorities of today’s consumers (retirement savings, covering LTC costs, paying for dependents’ education, etc.).

LIMRA research also suggests that although people appreciate the broader access to life insurance digital advances has provided them, they still yearn for human connection. Life insurers and financial professionals need to maintain a balance between adopting new technologies — particularly AI — and sustaining the human relationship that consumers desire.

- Consumers want to use technology to start learning about life insurance, but many say they want to talk to an expert (especially younger adults).

- They like the idea of a product that offers living benefits, but also say they want simpler, easy-to-understand products.

- They want a faster, easier process, but worry about privacy and want to work with a professional to make sure they are making the right decisions.

Technology is opening so many opportunities to expand and improve distribution, introduce new products, and engage a wider audience. But life insurance also has always been a relationship-based industry. Maintaining that balance will be crucial to the industry’s future success.

To watch the full Industry Insights with Bryan Hodgens episode, visit Understanding the Elusive Life Insurance Consumer.