Media Contacts

Helen Eng

LIMRA Retirement Public Relations/Social Media Lead

Work Phone: (860) 285-7834

2/26/2026

The workplace benefits market is entering a period of transition as economic conditions shift and employers rethink how they attract and retain talent. New LIMRA research examines how slowing growth, rising costs and evolving employee expectations are reshaping the outlook for workplace insurance products in 2026.

The post‑pandemic recovery brought an economic surge few could anticipate. Strong employment gains and rising wages created a sense of stability across the labor market. But the economic environment is shifting, affecting the dynamics of workplace benefits.

Weakening Job Market and Rising Costs Create Headwinds

After unemployment spiked to 14% in March 2020, employers spent 2022 and 2023 navigating an extremely tight labor market. Wages rose, benefit offerings expanded and competition for talent intensified. Starting in 2025, the unemployment rate began to rise. While still lower than 2016 levels (4.9%), employers began to focus on retention over recruitment. In addition, economic uncertainty and rising operating costs are constraining the resources employers can devote to compensation and benefits.

One of the biggest pressures is the cost of benefits themselves. Historically, benefit costs have been the most volatile component of compensation, often rising sharply during economic downturns. Health care costs continue to climb, and LIMRA’s analysis projects an 8% increase in 2026 without plan design changes. As health care consumes a larger share of compensation budgets, employers may shift more costs to workers or scale back other offerings. LIMRA’s Benefits Employee Attitude Tracker (BEAT) study shows workers already prioritize health, dental and vision coverage, often sacrificing “extras” to afford these essentials.

At the same time, persistent inflation continues to erode household budgets. Many workers report that rising prices still outpace their wage gains, leaving less room for other benefits, like life insurance, disability insurance and critical illness. While LIMRA research shows workers value non-medical insurance benefits more than ever, their ability to pay for them is under pressure.

Still, there are reasons for optimism. COVID‑19 fundamentally reshaped how workers think about financial protection.

“Our research shows workplace benefits are a priority for a large majority of employers and workers. In fact, 84% of employers believe benefits are critical in attracting and retaining workers and 83% of workers expect to have a wide variety of benefits available to them,” said Grace Rafferty, corporate vice president and director of LIMRA Workplace Benefits Research. “Although the pandemic enhanced awareness of the value and the need for insurance benefits, we've seen that urgency decline over time.”

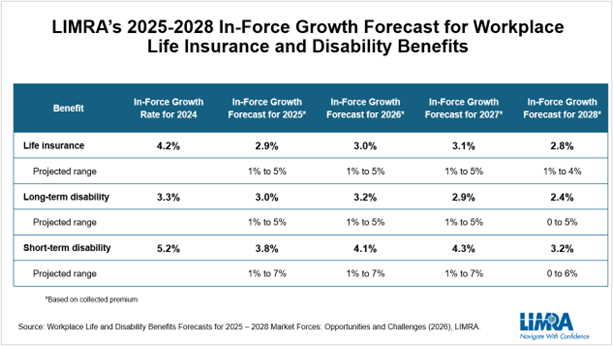

LIMRA Forecasts Muted Growth in Workplace Benefits in 2026-2028

As the U.S. economy cools from the post-pandemic recovery and employment growth is projected to fall to under 1% from 2026 to 2028, LIMRA forecasts slower in‑force premium growth for life and disability products through 2028. Life insurance in‑force premium growth is expected to fall below historical averages, while long‑term and short‑term disability premiums should remain closer to recent norms.

Innovation Can Spur New Opportunities and Growth

Several noneconomic factors are creating new opportunities. Employers still need competitive benefits packages to attract and retain top talent. Workers increasingly value flexibility, well‑being, and financial security. Advances in technology — from data analytics to AI — are enabling more personalized benefit recommendations and communications.

LIMRA research consistently shows employees favor receiving communications about their benefits throughout the year, rather than just prior to open enrollment. New technologies can help benefits providers and employers personalize communications to workers.

“Our research finds workers of different generations and life stages have distinct benefit priorities. Older generations tend to focus on health-related benefits, like disability and long-term care insurance, while younger workers prioritize life insurance, mental health benefits and caregiving support as they face raising their children and caring for their aging parents and grandparents,” said Bryan Hodgens, senior vice president and head of LIMRA. “There's a lot of opportunity to personalize and customize benefits and communications to improve worker participation.”

Ultimately, the market is transitioning out of a period where economic momentum did much of the heavy lifting. Growth over the next few years will depend less on tailwinds and more on innovation — in product design, enrollment strategies and communication. The demand is there. The challenge, and opportunity, lies in meeting it.

To learn more, watch the latest Industry Insights with Bryan Hodgens: Workplace Benefits Face New Environment in 2026.

LIMRA Retirement Public Relations/Social Media Lead

Work Phone: (860) 285-7834