Media Contacts

Helen Eng

LIMRA Retirement Public Relations/Social Media Lead

Work Phone: (860) 285-7834

6/26/2025

WINDSOR, Conn., June 26, 2025 — Although new LIMRA research shows employers plan to expand their benefit offerings over the next five years, softening economic conditions likely prompted employers to pause or pull back on their benefits packages in the first quarter of 2025.

“Over the past couple of years, workplace insurance sales have been strong, likely due to higher worker awareness about their need for coverage and employers choosing to offer a competitive benefits package to attract and retain the best workers in a very tight job market,” said Patrick Leary, corporate vice president and director of LIMRA’s workplace benefits research program. “As we expected, workplace insurance sales are beginning to normalize to pre-pandemic levels, resulting in lower sales this quarter.”

“Over the past couple of years, workplace insurance sales have been strong, likely due to higher worker awareness about their need for coverage and employers choosing to offer a competitive benefits package to attract and retain the best workers in a very tight job market,” said Patrick Leary, corporate vice president and director of LIMRA’s workplace benefits research program. “As we expected, workplace insurance sales are beginning to normalize to pre-pandemic levels, resulting in lower sales this quarter.”

Life Insurance

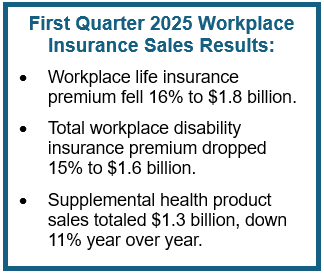

In the first quarter 2025, total workplace life insurance new premium fell 16% to $1.8 billion year-over-year. Over 6 in 10 participating carriers reported declines.

Although new premium for both term and permanent products broadly dropped 16% in the first quarter, whole life premium improved 6% during the first three months of the year. Group life insurance premium, which represent 93% of the market fell 16%, while individual sales were down 8%.

Disability Insurance

Total workplace disability insurance new premium was $1.6 billion in first quarter 2025, a 15% decline year-over-year. Short-term disability insurance new premium fell 13% and long-term disability insurance premium fell 16%.

Supplemental Health Insurance

Following two consecutive years of workplace supplemental health product sales growth― accident, critical illness, cancer, hospital indemnity, and other supplemental health insurance products* ― first quarter 2025 sales totaled $1.3 billion in new annualized premium, down 11% from the nearly $1.5 billion collected in the first quarter 2024.

Accounting for 95% of all new supplemental health premium in first quarter 2025, the major product lines of accident, critical illness and hospital indemnity insurance posted drops in sales, compared with results from the first quarter of 2024.

Group workplace and individual workplace supplemental health product sales accounted for 88% and 12% of all new premium, respectively. Group workplace supplemental health products fell 12%, while individual worksite sales declined 3%.

LIMRA’s workplace benefits sales surveys for life insurance, disability insurance and supplemental health represent more than 90% of their respective annualized premium markets.

You can find the latest data table with U.S. workplace sales trends in LIMRA’s Fact Tank.

-end-

*“Other supplemental health products” represents products that do not fit the other categories, such as gap insurance, minimum essential coverage plans, limited benefit medical, and heart/stroke products.

About LIMRA

Serving the industry since 1916, LIMRA offers industry knowledge, insights, connections, and solutions to help more than 700 member organizations navigate change with confidence. Visit LIMRA at www.limra.com.

LIMRA Retirement Public Relations/Social Media Lead

Work Phone: (860) 285-7834