Media Contacts

Helen Eng

LIMRA Retirement Public Relations/Social Media Lead

Work Phone: (860) 285-7834

10/29/2025

RILA quarterly sales surpass $20 billion for the first time, setting a new sales record.

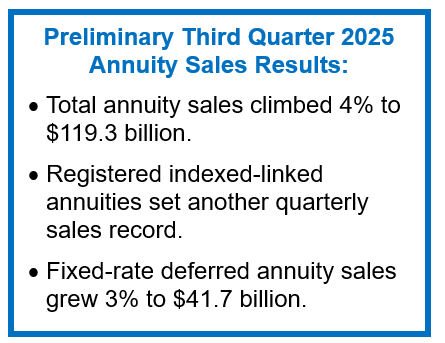

WINDSOR, Conn., Oct 29, 2025—Total U.S. annuity sales increased 4% to $119.3 billion in the third quarter of 2025, setting yet another quarterly sales record. This marks the eighth consecutive quarter of $100+ billion in sales.

Year to date (YTD), annuity sales totaled $345.0 billion, up 4% year-over-year. This is the highest total ever recorded in a nine-month period, according to preliminary results from LIMRA’s U.S. Individual Annuity Sales Survey., which represents 89% of the total U.S. annuity market.

“Registered annuity products – traditional variable annuities and registered index-linked annuities – posted double-digit growth, contributing to the overall growth in quarterly sales. Despite continued market volatility, the equity market's overall performance attracted investors looking to counter persistent inflation,” said Bryan Hodgens, senior vice president and head of LIMRA research. “Although the Federal Reserve’s expected interest rate cuts will likely dampen fixed annuity sales gains, LIMRA is projecting annuity sales to surpass $450 billion in 2025.”

continued market volatility, the equity market's overall performance attracted investors looking to counter persistent inflation,” said Bryan Hodgens, senior vice president and head of LIMRA research. “Although the Federal Reserve’s expected interest rate cuts will likely dampen fixed annuity sales gains, LIMRA is projecting annuity sales to surpass $450 billion in 2025.”

Registered Index-Linked Annuities

Registered index-linked annuity (RILA) set a new quarterly sales record. In the third quarter of 2025, RILA sales were $20.6 billion, 20% higher than the prior year and ten times the sales recorded a decade ago for this product line. In the first three quarters of 2025, RILA sales increased 18% year over year to $57.3 billion.

“Market volatility moderated in the third quarter, and equity markets have logged double-digit growth since the start of the year. This is a perfect environment for RILAs, which offer protected growth with attractive caps and participation rates aligned with equity market returns,” said Keith Golembiewski, assistant vice president and director of LIMRA Annuity Research. “This quarter, we saw three more companies introduce new RILA products, a new carrier enter the RILA market, and several additional firms enhance their existing offerings. LIMRA expects the growth trajectory for RILA will continue for the foreseeable future.”

Traditional Variable Annuities

Traditional variable annuity sales rebounded from the second quarter. The third quarter sales were $16.7 billion, up 11% year over year. YTD, traditional VA sales were $46.9 billion, 6% higher than the same period in 2024.

Fixed-Rate Deferred

Total fixed-rate deferred annuity (FRD) sales were $41.7 billion in the third quarter, 3% higher than third quarter 2024 sales. YTD, FRD annuity sales increased 2% year over year to $126.6 billion.

“Although lower interest rates may slightly diminish demand for FRD products in future quarters, sales have more than doubled from just a few years ago,” noted Golembiewski. “We believe FRDs, which continue to offer higher crediting rates than CDs, have become an attractive, short-term solution for risk-adverse investors and their advisors looking for protected investment growth.”

Fixed Indexed Annuities

Fixed indexed annuity (FIA) sales fell 6% year over year to $33.2 billion in the third quarter. YTD, FIA sales were $93.8 billion, sliding 1% from record results posted in the nine months of 2024.

Income Annuities

After a sluggish start in 2025, single premium immediate annuity (SPIA) sales increased 6% in the third quarter to $3.7 billion. However, YTD SPIA sales remained 2% below sales recorded in the first three quarters of 2024.

Deferred income annuity (DIA) sales were $1.3 billion in the third quarter, down 5% year over year. YTD, DIA product sales fell 11% to $3.4 billion. Despite the decline this quarter, DIA sales are consistently three times the sales posted five years ago.

“Consistently, LIMRA research finds a majority of consumers worry about running out of money in retirement. For Generation X consumers* — who are less likely than older generations to have a pension — nearly 6 in 10 are concerned about outliving their savings,” said Hodgens. “While recent favorable economic conditions have helped to double annuity sales over the past five years, LIMRA believes consumers’ greater understanding of the value of guaranteed income will keep demand relatively steady, regardless of shifting economic conditions. The Alliance for Lifetime Income by LIMRA will continue the mission of helping Americans understand the role annuities play in achieving financial security in retirement.”

Preliminary third quarter 2025 annuity industry estimates are based on monthly reporting. A summary of the results can be found in LIMRA’s Fact Tank.

The top 20 rankings of total, variable and fixed annuity carriers for the first nine months of 2025 will be available in late November, following the last of the earnings calls for the participating carriers.

*Working adults ages 45-60 with at least $150,000 in household assets – Source: 2025 Protected Retirement Income and Planning (PRIP) Study Chapter 2: Family First, Health Care and Caregiving Worries, Gen X Concerns (2025), Alliance for Lifetime Income by LIMRA

LIMRA Retirement Public Relations/Social Media Lead

Work Phone: (860) 285-7834