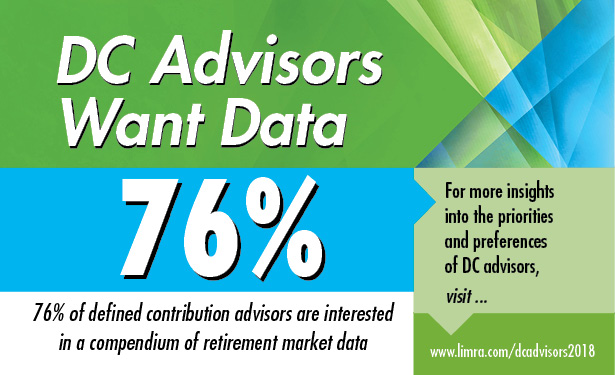

Defined contribution advisors are unique in the financial advisor community. See how their preferences and priorities further differ based on their DC assets under advisement (AUA) and type of DC compensation.

Deb Dupont 1/28/2019

Defined contribution advisors are unique in the financial advisor community. See how their preferences and priorities further differ based on their DC assets under advisement (AUA) and type of DC compensation.

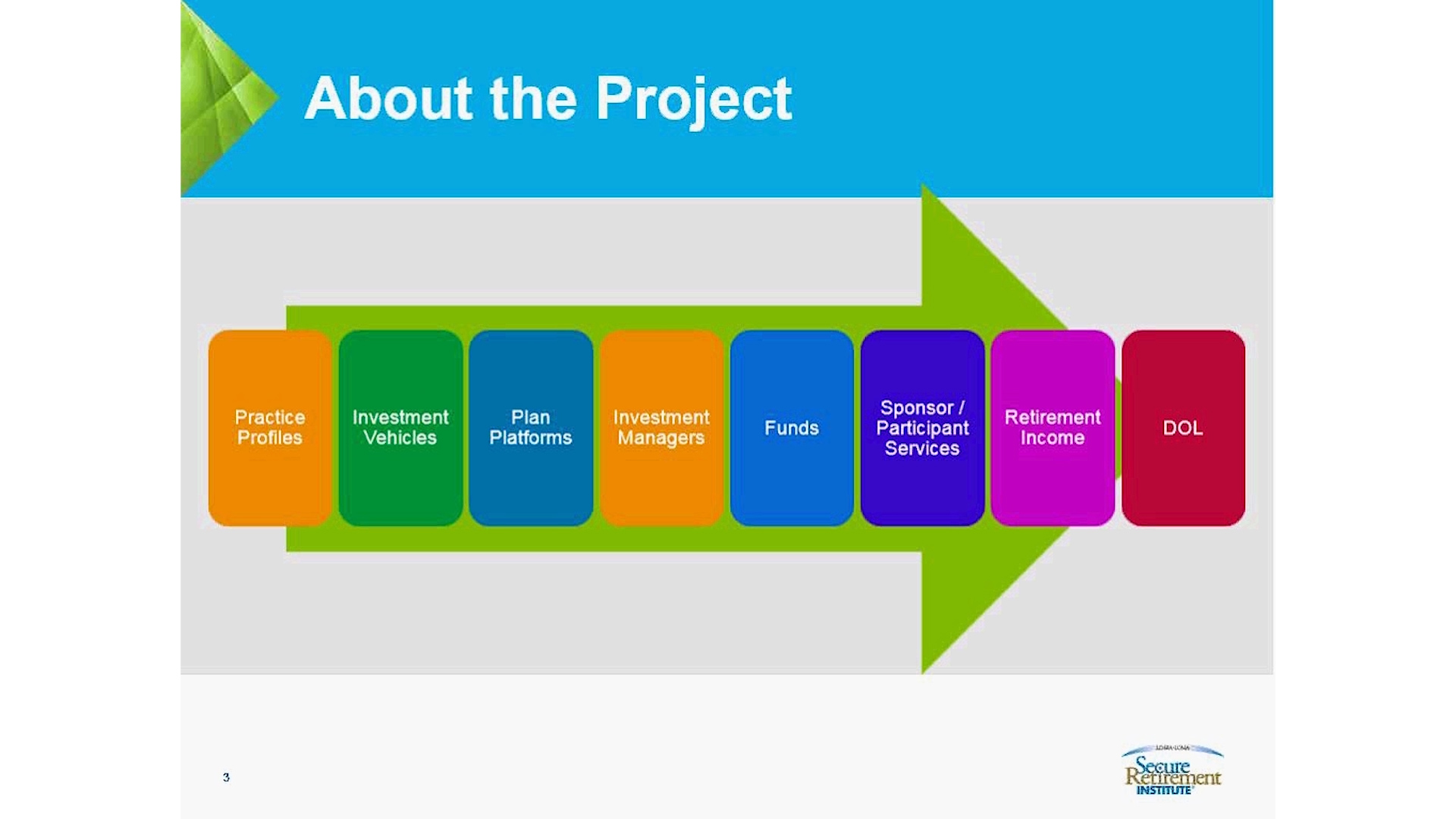

Advisors who sell defined contribution (DC) plans and services, and consult on DC investment menus, represent a unique subset of the financial advisor community. Even within this universe — advisors who “play” in the DC space — there are subtle distinctions among practices.

This research examines advisors based on their DC assets under advisement (AUA) and the way they are compensated for their DC business (fees and/or commissions). It looks at their preferences and requirements for investment platforms and services, what they look for in provider partners, and how they evaluate funds for their DC clients, offering important insights for providers who are looking to partner or deepen their relationships with this critical audience — which represents a “gateway” to DC plan sales and clients.

Service to sponsors and participants is of paramount importance to plan advisors, and in order to better support their efforts, knowing how they craft their own service offering is paramount.

Advisors who sell DC plans are unique. Learn more about the services they offer to plans and participants, and explore how your company can add value as a provider of choice.

The 2026 Retirement Income Readiness Report examines retirement preparedness, retirement income planning, financial confidence, protected lifetime income, and the factors that help pre-retirees and retirees achieve long-term financial security.

The inaugural LIMRA Retirement Plan Income Annuity Benchmark offers a first-of-its-kind view into the size and growth of the in-plan annuity market.

LIMRA’s latest study updates more than six decades of life insurance ownership trends, adding new estimates to better reflect today’s coverage landscape. Technical Report now available.

Benchmark sales for a range of fixed and segregated fund contracts; by distribution system and province. New Q4 2025 GLIMPSE.

Deb Dupont is responsible for LIMRA’s institutional (retirement plans) retirement research program. She conducts and supervises research, benchmark reporting, and study groups focused on the issues and trends faced by constituents of the defined contribution industry. She also provides guidance and thought leadership in helping LIMRA's member firms better understand the opportunities available for improving delivery of institutional retirement solutions.

Prior to joining LIMRA in 2014, Deb was the Director of ING's Retirement Research Institute (the Institute), where she created, managed, and published a research platform that included work focusing on multi-cultural, generational, and gender-based analyses of retirement behaviors, and also published insights and analyses of ING's own cross-defined contribution (i.e., across employment sectors) participant base. Deb's work has been recognized for effectiveness and quality by some of the most prestigious awards in the financial services and communications industries, including the Insurance and Financial Communicators' Association and the International Association of Business Communicators. She is a graduate of the University of Connecticut.

Assistant Vice President Workplace Benefits Research, Institutional Retirement

LIMRA and LOMA

ddupont@limra.com

Don't You Forget About Me: There's Market Potential in Gen X

Access information regarding recent retirement specific research, educational resources, industry news and much more.

Understanding the advisors who sell Defined Contribution plans is critical for companies – particularly recordkeepers and other service providers – who want to succeed in the DC space.