LIMRA worked with the Society of Actuaries and Oliver Wyman to conduct a series of short surveys on the COVID-19 pandemic and its potential effects on the insurance industry.

The COVID-19 pandemic has resulted in social-distancing practices and volatile market conditions that have caused disruptions in many life insurance companies’ processes.

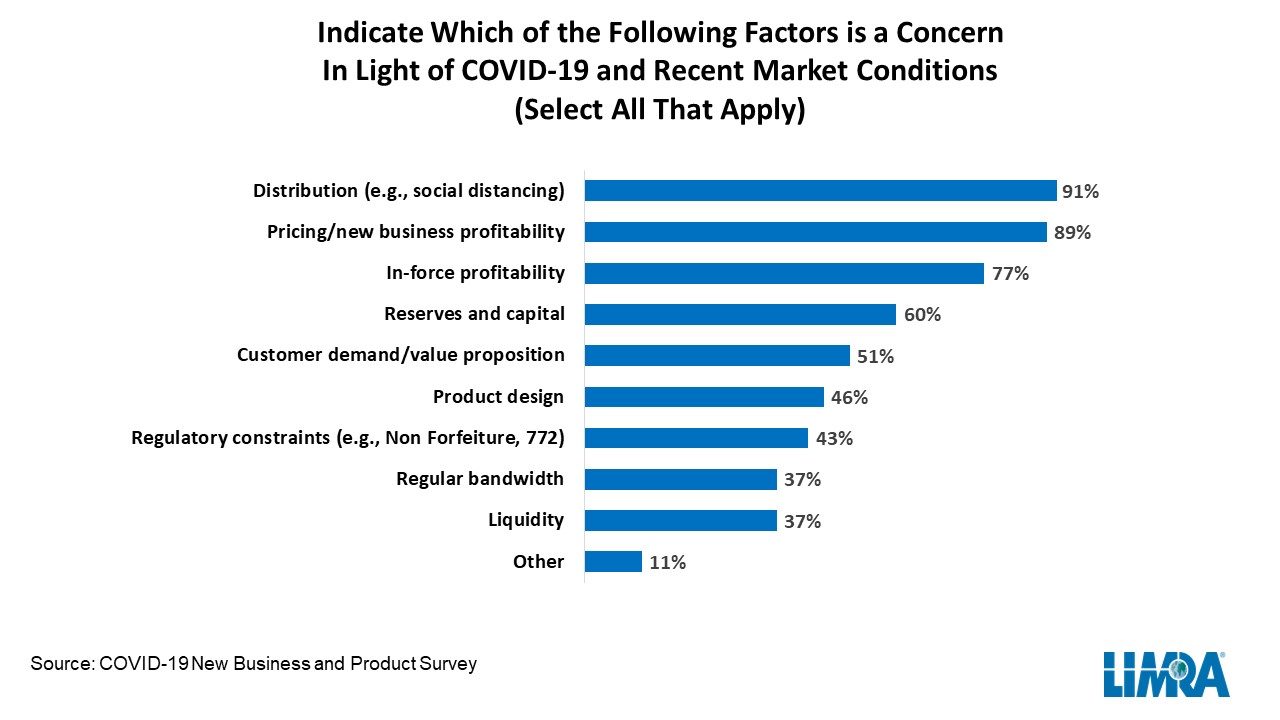

About 90% of the companies rated distribution/social distancing and pricing/new business profitability (89%) as a concern and 77% listed in-force profitability.

“Companies have had to be nimble in making adjustments where needed to their product rates and pricing,” said Marianne Purushotham, research actuary, LIMRA, who co-authored the survey.

Depending on the product, various factors contribute to companies’ current pricing challenges:

- Increased cost of hedging and declining government bond rates were the biggest concerns for variable annuity writers;

- Declining government bond rates and rising credit spreads/default risk topped the concerns for fixed and/or fixed indexed annuity writers;

- Underwriting uncertainty, declining government bond rates, and increased/uncertain mortality/morbidity were the primary concerns for term life writers; and

- Declining government bond rates and underwriting uncertainty presented the biggest challenges for permanent life insurers.

To manage these new economic challenges companies have taken various steps:

- 58% of respondents have increased the frequency of reviews for pricing/caps/crediting rates;

- Two-thirds of respondents have increased monitoring of new business volumes and almost half (47%) have increased their monitoring of new business profitability;

- About half of respondents have adjusted non-guaranteed elements and about 30% have adjusted guarantees;

- Almost 6 in 10 respondents have restricted life and health products for recent travel to specific countries; and

- About one-third have updated their long-term interest rate assumptions.

There have also been changes in underwriting for life insurance products. Two-thirds of respondents have changed their underwriting process to address the lack of access to traditional paramedical testing. Of those who have changed, about two-thirds are using attending physician statements in place of fluid requirements, two-thirds are increasing automated/accelerated underwriting limits, and about one half are using telephone or FaceTime screenings.

The study results indicate life insurers are adapting to the new economic conditions and physical limitations brought on by the COVID-19 pandemic. These changes will enable companies to continue to provide Americans the protection products they need to secure their financial future.