This week, LIMRA updated its sales forecast for U.S. retail life insurance sales for 2021. Since October 2020, when the original forecast was published, three COVID-19 vaccines were given emergency approval and distributed, two federal relief packages were passed and a last-minute change to life insurance tax law was implemented. These factors, coupled with stronger economic conditions and unprecedented consumer interest in life insurance, have led LIMRA to improve its 2021 sales forecast.

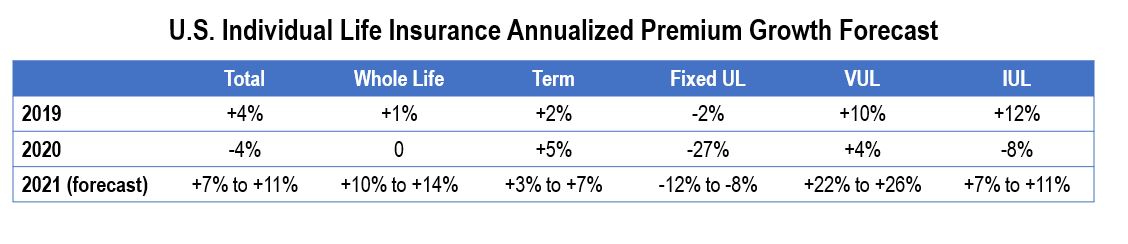

In the first quarter 2021, total individual premium jumped 15% and the number of policies sold increased a record-breaking 11%. With that backdrop, LIMRA expects the U.S. life insurance market to grow between 7% and 11% in 2021, compared with 2020 results. All product lines’ premiums except fixed universal life (UL) are expected to improve, with whole life, indexed UL and variable UL projected to experience the largest growth.

Whole Life: Increased consumer interest in life insurance and an expansion of accelerated underwriting programs have helped sales across all distribution channels for whole life. We are expecting increased consumer interest in life insurance to continue through the rest of 2021. This will result in double-digit premium growth in 2021.

Term Life: Following the strong growth in 2020 (up 5%), continued strong consumer interest and online availability will help term premium have another strong year in 2021. LIMRA is forecasting premium growth to be as high as 7% in 2021.

Variable UL (VUL): While this product represents a small fraction of the overall U.S. life insurance market, sales have been quite strong, driven by protection-focused product sales. VUL new premium is expected to increase more than 20% in 2021.

Indexed UL (IUL): After an 8% drop in 2020, LIMRA predicts indexed UL sales to grow as much as 11% in 2021. Slowly improving interest rates and lower volatility will bolster IUL sales, along with the potential for a positive impact from the change in life insurance tax law, particularly on accumulation-focused products.

Fixed UL: While interest rates are in a much better place than they were six months ago, they continue to make it difficult for life insurers to offer secondary guarantees, making these products less competitive in the market. LIMRA forecasts fixed UL new premium to continue to decline around 8% to 12% in 2021.