LIMRA Retirement Research

Matthew Drinkwater, Ph.D., FSRI, FLMI, AFSI, PCS 4/20/2017

DConversations - Automatic Portability: A New Approach to Addressing Retirement Plan 'Leakage'

How will companies adapt their call centers and asset retention programs to comply with the DOL rule?

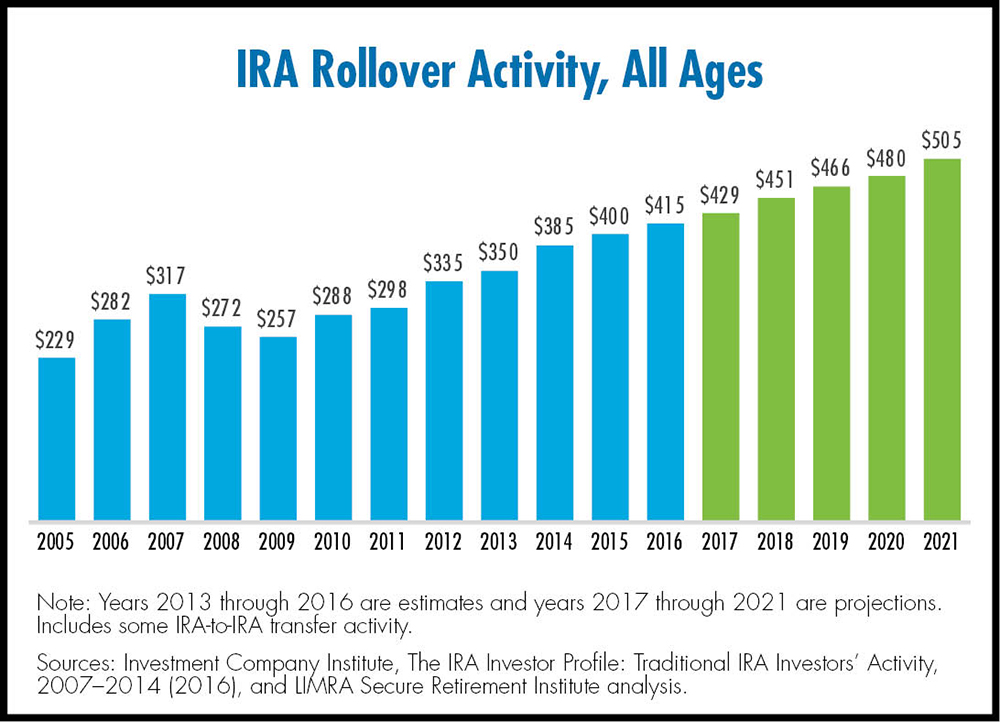

What’s in store for the contributory and rollover IRA markets?

Why aren’t more workers contributing to IRAs?

Is retirement saving being crowded out by other saving and spending needs?

Find out how employers describe plan distribution options available to retiring employees, whether they make specific recommendations, and what they would prefer retirees do with their plan balances.

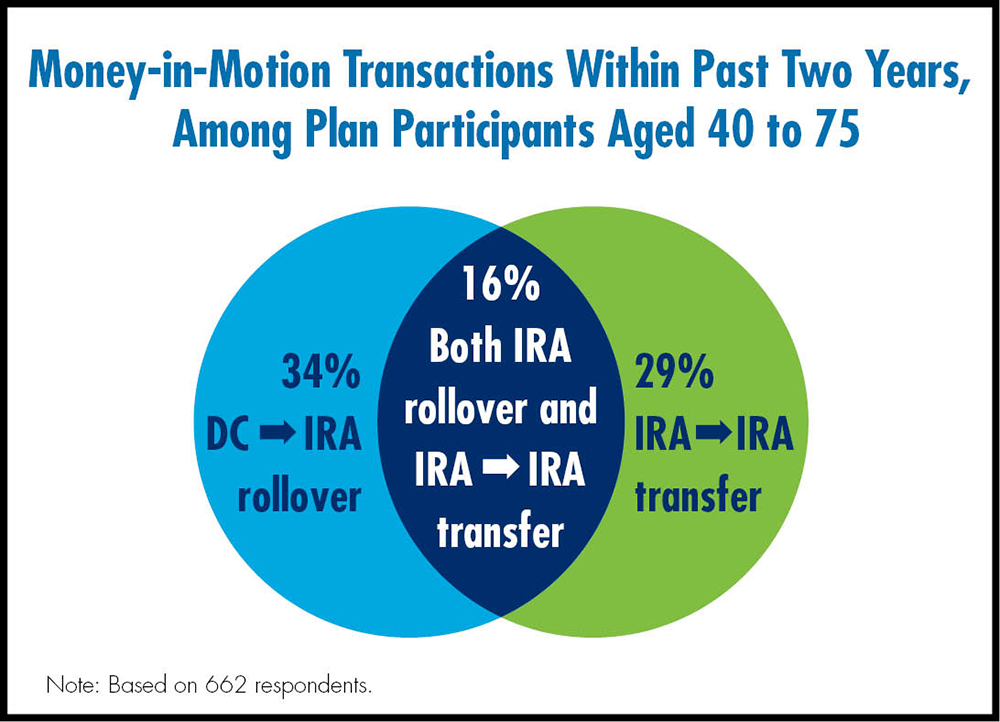

Are consolidation, control, and convenience still driving rollover decisions? View our most recent findings to discover successful asset retention strategies.

Matt Drinkwater, who joined LIMRA in 1999, leads the annuity and retirement income primary research program. He has led the creation of several major studies of retirement planning, retirement income planning and management, and consumer preferences for receiving advice. Drinkwater has directed several institutional retirement research projects, including studies of asset retention and the rollover market. His research on annuities has encompassed in-depth studies of product features, buyer and owner characteristics, persistency, and living benefit utilization.

He is a graduate of Trinity College (Hartford, CT) and holds a doctorate in psychology from Brown University.

Corporate Vice President, Annuity and Retirement Income Research

LIMRA and LOMA

mdrinkwater@limra.com