LIMRA Life Insurance Research

Deb Dupont 7/18/2017

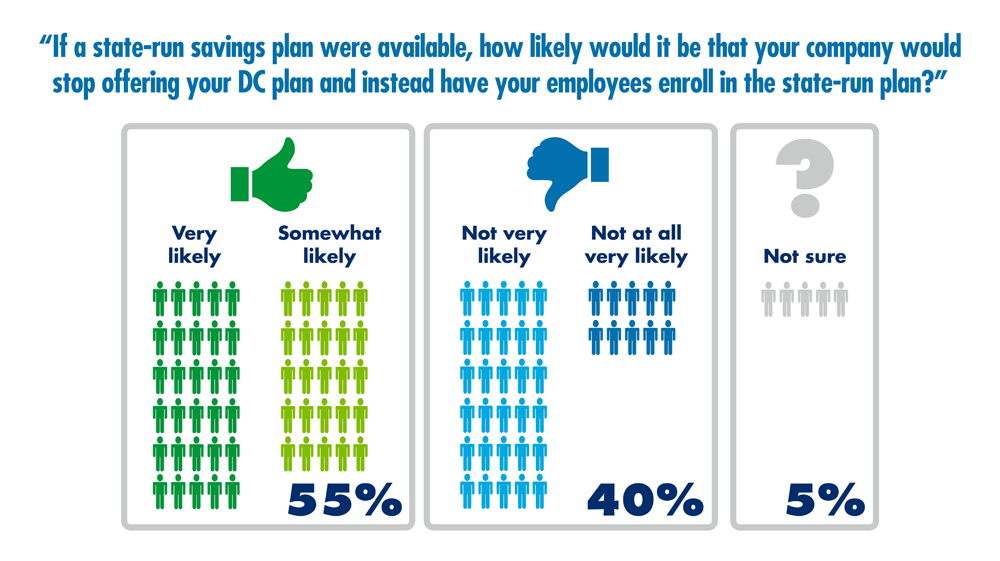

The Department of Labor estimates that 38 percent of private sector workers do not have access to a Defined Contribution (DC) plan. Making worksite savings available to more workers is a critical first step in helping resolve the issue of how workers invest and save for retirement via the workplace. Lack of access is especially pronounced among employees of smaller companies, and can be complicated by questions of full- or part-time working status, or tenure with a given employer. The Federal government and more than half of the states have turned their attention to the lack of DC programs in so many workplaces, with proposals, studies and legislation various stages to enable workplace savings.

In 2016, the LIMRA Secure Retirement Institute conducted two surveys – one of workers and another of employers who currently sponsor DC plans. Each initiative included a battery of questions designed to better understand the two stakeholders who are most directly affected by these efforts at the state levels.

A new mantra for the retirement industry seems to be taking hold: driving successful retirement outcomes for plan participants.

LIMRA’s latest study updates more than six decades of life insurance ownership trends, adding new estimates to better reflect today’s coverage landscape. Technical Report now available.

Consumers want life insurance that is simple, flexible, and easy to integrate into their financial lives. Explore insights from the 2026 Insurance Barometer Study.

Is life insurance evolving as fast as consumer expectations? Insights from the 2026 Insurance Barometer Study reveal today’s consumers want more – more flexibility, more relevance, and more value.

Deb Dupont is responsible for LIMRA’s institutional (retirement plans) retirement research program. She conducts and supervises research, benchmark reporting, and study groups focused on the issues and trends faced by constituents of the defined contribution industry. She also provides guidance and thought leadership in helping LIMRA's member firms better understand the opportunities available for improving delivery of institutional retirement solutions.

Prior to joining LIMRA in 2014, Deb was the Director of ING's Retirement Research Institute (the Institute), where she created, managed, and published a research platform that included work focusing on multi-cultural, generational, and gender-based analyses of retirement behaviors, and also published insights and analyses of ING's own cross-defined contribution (i.e., across employment sectors) participant base. Deb's work has been recognized for effectiveness and quality by some of the most prestigious awards in the financial services and communications industries, including the Insurance and Financial Communicators' Association and the International Association of Business Communicators. She is a graduate of the University of Connecticut.

Assistant Vice President Workplace Benefits Research, Institutional Retirement

LIMRA and LOMA

ddupont@limra.com