Strategic Consolidation Reshaping Distribution

Strategic Consolidation Reshaping Distribution

June 2026

Financial services distribution is in one of the most transformative periods in its history. Strategic consolidation — fueled by accelerated mergers and acquisitions (M&A) activity and private equity (PE) investment — is reshaping the competitive landscape at unprecedented speed.

(Dollars in billions — bank, advisor, consultant, value‑added partner (BACV))

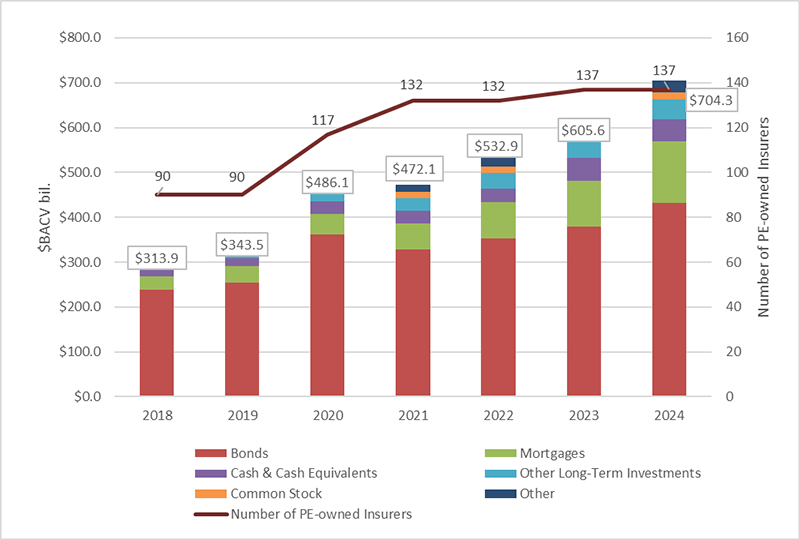

The NAIC Capital Markets Special Report Private Equity-Owned YE2024 states that private equity’s entry into the insurance sector was initially catalyzed by the industry’s stable, long‑duration cash flows during a prolonged low‑interest‑rate environment (2007-2009). Although PE firms have invested broadly across the insurance industry, they have been particularly interested in insurers with long-term liabilities, such as annuities and life insurance, that generate stable cash flows from premiums. In turn, this provides PE firms with the opportunity to redeploy life insurers’ relatively stable, low-cost funds into higher-return funds and investments managed by the PE firm and its affiliates. This growth, starting in 2009, accelerated significantly between 2018–2024.

Under PE ownership, insurers are positioned within broader capital markets and investment ecosystems, enabling access to sophisticated asset management and investment capabilities as well as operating infrastructure. As a result, private-capital-backed insurers have scaled assets at rates exceeding 20% annually, with assets totaling nearly $1.5 trillion in 2025, according to a 2026 McKinsey report. Beyond U.S. insurers, PE firms are also investing in insurance platforms, intermediary firms and wealth management companies.

The growth in PE investment in the financial services industry has gained the attention of U.S. state insurance regulators, whose mandate includes protecting policyholders and maintaining the financial stability of insurers. A 2024 Mayer Brown report states that regulators believe current guidance may not fully capture issues related to offshore reinsurance arrangements, capital reserve and adequacy requirements, affiliation and control structure disclosures, structured assets, and the use of sidecar vehicles. Of note, this extends beyond PE-owned insurers to any insurer engaging in these activities.

Looking to 2026 and beyond, PE firms signal that they will remain active in insurance and wealth management.

Alongside these trends, we have seen continued M&A activity in financial services over the last few years. In 2025, deal volume was down, but values increased, demonstrating continued activity that is larger in scale and more strategic in nature. A 2026 KPMG study confirms that this 2025 trend signals more strategic activity focused on prioritizing scale, platform building, and capabilities expansion to enable business‑model transformation.

M&As have become a primary mechanism for capability acceleration, enabling firms to efficiently compete in the evolving financial services landscape — currently defined by higher regulatory costs, thinning margins, rapid product innovation, and evolving client expectations — thereby driving the convergence across insurance, asset management, and wealth management. To bring this industry dynamic to life, below are notable 2025 transactions, based on value and strategic intent:

On the heels of 2025’s value-driven deal activity, 2026 is proving to be another noteworthy year, with the March announcement of the Equitable–Corebridge merger creating a $1.5 trillion retirement, life, and wealth company with 12 million customers.

This reinforces that increasingly targeted distribution and operating-capability building are underway to create more sophisticated advisor platforms and tighter control of distribution. A 2026 McKinsey Report reveals that as distribution consolidates, a smaller number of partners now control a greater share of sales volume, while the insurers’ costs of distribution have remained elevated.

A 2024 McKinsey wealth management report finds that after years of consolidation, the financial services industry has reached a point where traditional distinctions between channels are increasingly becoming indistinct. Differences once defined by business model, affiliation, regulatory structure, product orientation, or ownership (e.g., wire houses, independent broker-dealers, registered investment advisors (RIAs), banks) are becoming less relevant as firms evolve toward more integrated platforms and operating models.

Amid this transformational change, Mayer Brown reinforces that regulators will continue to scrutinize PE investments in the insurance sector at both the state and federal levels. The NAIC, Bermuda Monetary Authority, and International Monetary Fund have rolled out initiatives and guidance on private equity’s growing role in the life insurance industry. U.S. policymakers will evaluate PE ownership through forums such as Senate hearings. As this continues to evolve, it will be important for the broader financial services industry to monitor and understand how policy and regulations have developed — and will continue to develop — over time.

June 2026 Subscribe

Strategic Consolidation Reshaping Distribution

Spotlight on MassMutual’s CMO Meghan Doscher

Annuity Awareness Month: Helping Overcome Barriers

Building the Future Workforce in the Era of AI

PEPs in Practice: Small Plan Advisors Are Least Familiar

Legacy Thinking: The Future Depends on a Mindset Shift

ADVERTORIAL: Life Insurance Applicants Willing to Use Patient Portals