The Elusive Consumer: Why Aren’t They Buying?

The Elusive Consumer: Why Aren’t They Buying?

Stephen Wood

Research Director, Markets Research

LIMRA and LOMA

July 2026

Those of us who watch sports hear the word “elusive” all the time: the elusive running back who slips through tacklers’ grasps, the elusive midfielder who dribbles through two well-placed defenders, the elusive winger who slips past a bodycheck to score the game-winning goal.

With life insurance, the elusive consumer is similar. They say they need and want life insurance, they can afford it, and most importantly, they’ve reached the stage of life when it makes the most sense to purchase it.

Yet they are not purchasing as many policies as the aspirational “plan to purchase” data suggest they will.

A look at self-reported life insurance ownership and the need-gap since 2011 shows a pattern and, perhaps, suggests that a new trend has recently begun.

The life insurance need-gap is a simple summation of consumers who are uninsured and say they need to be insured, plus those who have some life insurance and say they need more. Generally speaking, the higher the level of ownership, the fewer people report a need. The COVID-19 pandemic elevated need for about five years, although ownership plateaued in response rather than increasing.

The traditional life insurance policy buyer was married and had recently bought their first home and/or welcomed their first child. Dad worked while mom raised the family.

Today, fewer people are getting married, and those who do often do so later in life. Many couples are choosing to delay having children or eschewing parenthood altogether. Homebuying has been very difficult in the U.S. and Canada, and first-time buyers are typically much older than in the past. Increasingly, both partners are working equally.

These societal shifts have certainly impacted life insurance policy sales. In 2026, the rising cost of living is also certain to have at least a short-term impact. Life insurance is just not seen as a true necessity by millions of people.

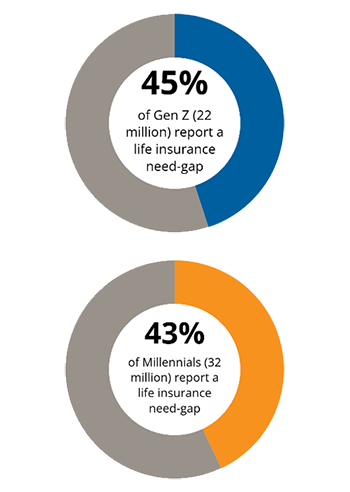

It is true that, at $17.5 billion in annualized premium, life insurance set yet another record in 2025. Policy count also increased 7% over 2024. But the elusive consumer remains, as many Generation Z and Millennial consumers are not purchasing variable universal life policies at the higher end of the spectrum, nor are they the typical market for final expense or preneed policies at the more affordable end.

Many of them may have a policy through their employer, but 55 million younger adults say they have a life insurance need-gap.

Simply put, they are online, on their smartphones or social media apps. Unfortunately for life insurance marketers, distributors and sellers, they are in these spaces in new and different ways than just a few years ago.

Today’s consumers are demanding a seamless physical/digital interface. Gone are the days of inputting “life insurance” into a search engine and landing on a company’s customer-facing website or life insurance calculator.

When someone asks a search engine or artificial intelligence (AI) tool about life insurance, they are typically given basic information. From there, they may either continue to probe AI, which may or may not result in a lead, or follow links — or simply move on (“scroll”). As a result, they will often be served life insurance advertising and other content.

They may be prompted to follow life insurers, financial influencers, and direct-to-consumer sellers. If they move to a different social media platform, they may intentionally seek more or different information to compare and contrast. They may ask generative AI more specific questions about their personal situation.

Today’s consumers home in on the answers they seek via multiple platforms, quickly, and often with AI input.

At some point, armed with information from various searches, apps and crowdsourced opinions, they will often want to talk to a professional. This could happen in any number of ways, and it is here that the seamlessness between human and digital becomes important.

How will they find a company or an agent? Will that agent be local — human or AI? How will the consumer move from a social media app to this conversation?

In 2026 and beyond, the expectation is that these transitions will be fast, smooth and easy. With complicated products like life insurance, this is not always possible. However, an effort must be made.

It takes effort to cut through the noise of social media to be relevant, interesting and shareable. However, it is possible through short-form videos on YouTube, where over two-thirds of young adults go for financial information. Facebook (53% of Gen Z uses it for this purpose) is still utilized but attracts fewer young adult audiences than Instagram (58%) and TikTok (57%) (see Figure 2).

Increasingly, social media influencers and “fin-fluencers” are trusted — for better or for worse. Many are reputable, provide good information, and are, in the eyes of some, today’s “celebrity spokespeople.” It is difficult for many insurance companies with more than a hundred years of experience to adapt to this new world, but LIMRA data suggest it is becoming more and more imperative to do so.

Today’s young adults will likely remain elusive, simply because of their online behavior, societal changes, competing products, and economic concerns. However, if we lean into this apparent chaos, craft an intelligent AI strategy (understand what drives AI to push people to a company’s social media, website, local agent, or even brick-and-mortar locations), create relevant content where they are (YouTube, Facebook, Instagram, TikTok, etc.) and appeal to emotional and pricing concerns, we can better engage this group.

July 2026 Subscribe

LIMRA Financial Wellness Index: 2026 Update

Annuity Market: Looking Beyond Headline Sales

Spotlight on Shana Sood, CMCO at Prudential, ILI

Today’s Company-Owned Broker-Dealer Market Shifts

Longevity as a Distribution Issue: Lessons from Japan

Why One-and-Done Sales Training Falls Short

The Elusive Consumer: Why Aren't They Buying?